ASIC

Your margin is my opportunity

This report, and almost all the research you have read at Market Sentiment, was written on an M-series MacBook. Before 2020, laptop battery life was universally pathetic. Companies claimed 8+ hours and barely delivered 4. Apple changed everything with the M1 MacBook in 2020.

The jump in performance per watt was incredible. M chips did the same tasks Intel chips did at roughly a quarter of the power draw. The result: the M1 Air managed 15 to 18 hours of real use versus barely 8 hours on the Intel Air with the same battery capacity.

Apple achieved this with custom silicon. Intel could never build this chip for Apple because Intel had to serve everyone. Its processors carried decades of baggage and had to work in every Windows machine from a $300 Dell to a gaming rig, so they could not be optimized for one laptop or one operating system.

Apple’s decade long investment into custom silicon paid off — Mac revenue which was stagnated at ~$25B from 2017 to 2019 jumped 60% and touched ~$40B by 2022 before normalizing to $33B for the latest year.

This is not about laptops; It is that owning your silicon converts directly into performance per watt, and performance per watt converts directly into a product nobody else can build.

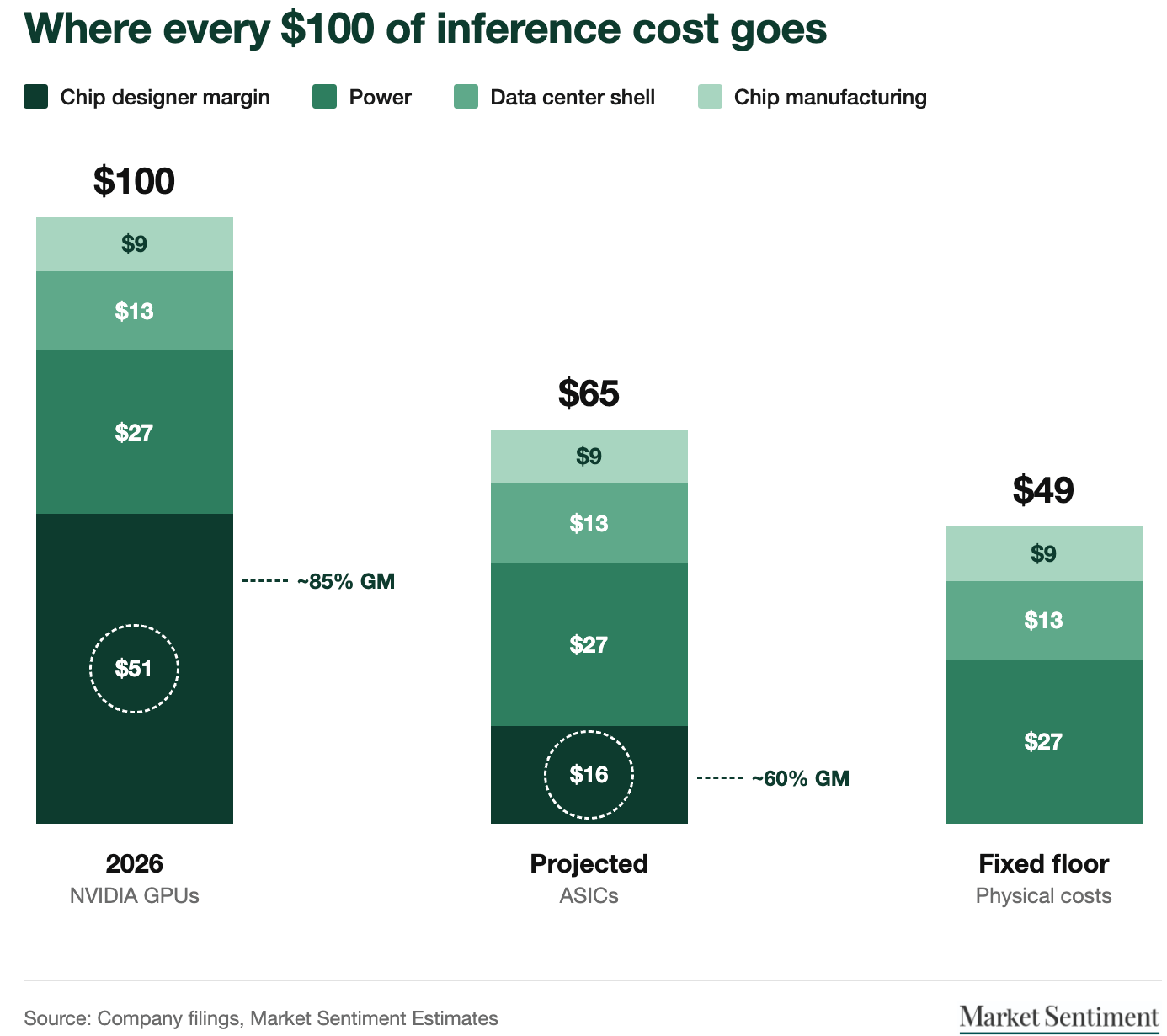

Nowhere is this now more important than AI. Our estimates show that for every $100 of inference cost, hyperscalers currently hand roughly half to Nvidia. This eye-watering 85% gross margin Nvidia charges for its AI chips is currently the single largest tax on the AI buildout, and it is a tax you can escape by designing your own silicon.

Market Sentiment dives deep into the bottlenecks of the AI world. Join 46,000 other investors to make sure you don’t miss our next briefing.

What is an ASIC?

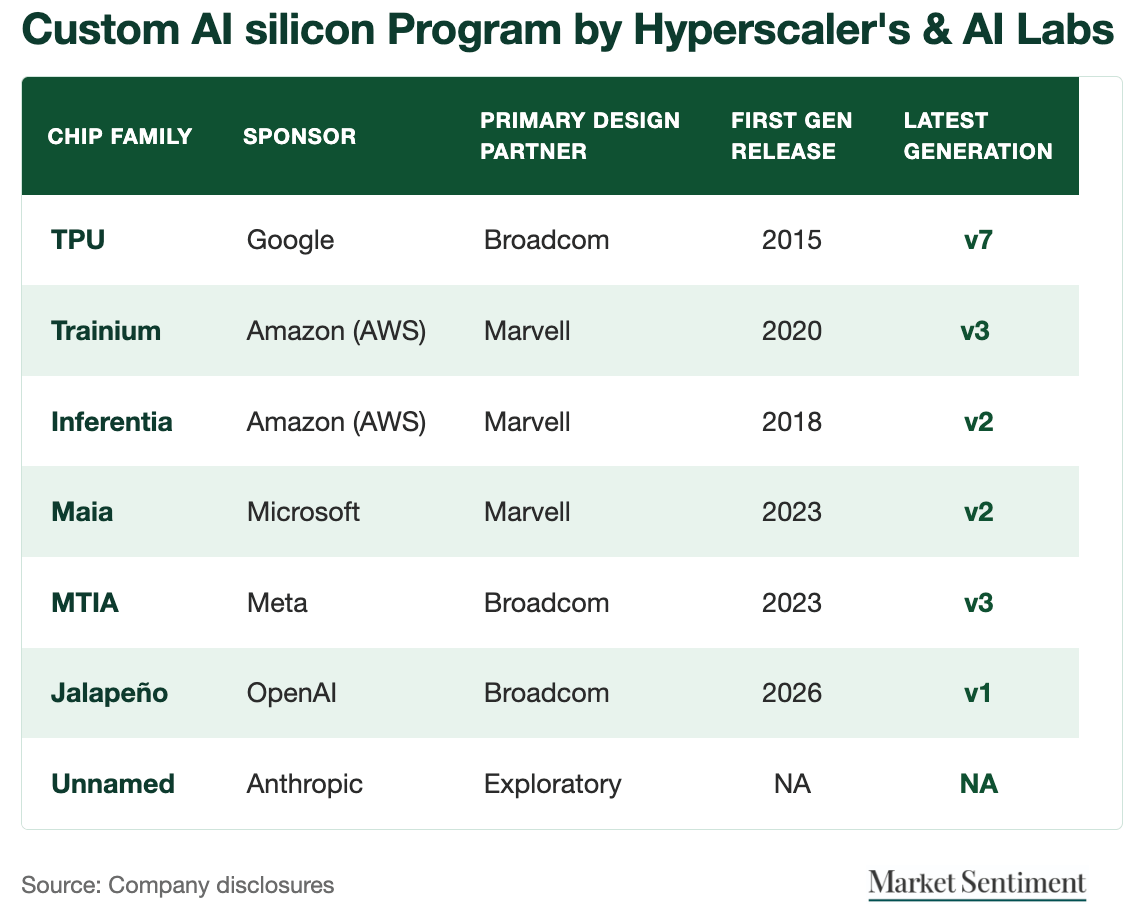

ASIC stands for Application Specific Integrated Circuit. It is a chip designed by one company for its own specific use case, rather than sold on the open market. Examples include:

The Apple M series chips we just discussed

Google’s TPU AI processor

Amazon’s Trainium 3 AI processor

Nokia’s ReefShark base station processor

If you are wondering how these differ from Nvidia or AMD GPUs: a GPU is a Swiss Army knife whereas an ASIC is a scalpel.

Nvidia builds its GPUs to run anything. Training, inference, any model architecture for text, vision, protein or physics, in any precision format. That flexibility comes at a price. A meaningful share of every GPU die is spent on circuitry your specific workload will never touch.

An ASIC flips the trade. You strip out everything except what your workload needs and pour the entire silicon budget into exactly that. Bitcoin mining chips are the purest example. They compute one hashing function billions of times a second and can do literally nothing else. Not even a calculator app would run on one.

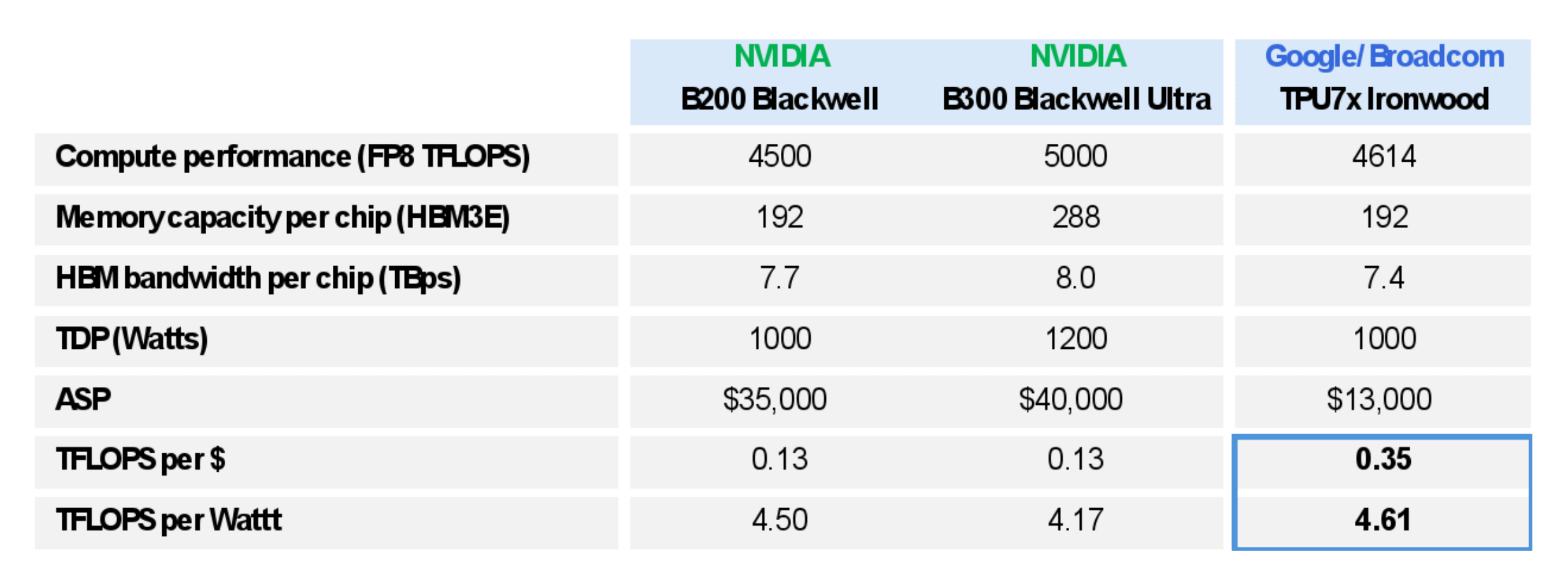

The AI versions apply the same logic to neural networks. The result is 2 to 3x better performance per watt and real savings on silicon cost: Google's TPU7x matches NVIDIA's B200 on raw compute at roughly a third of the price: ~$13,000 per TPU vs $35,000.

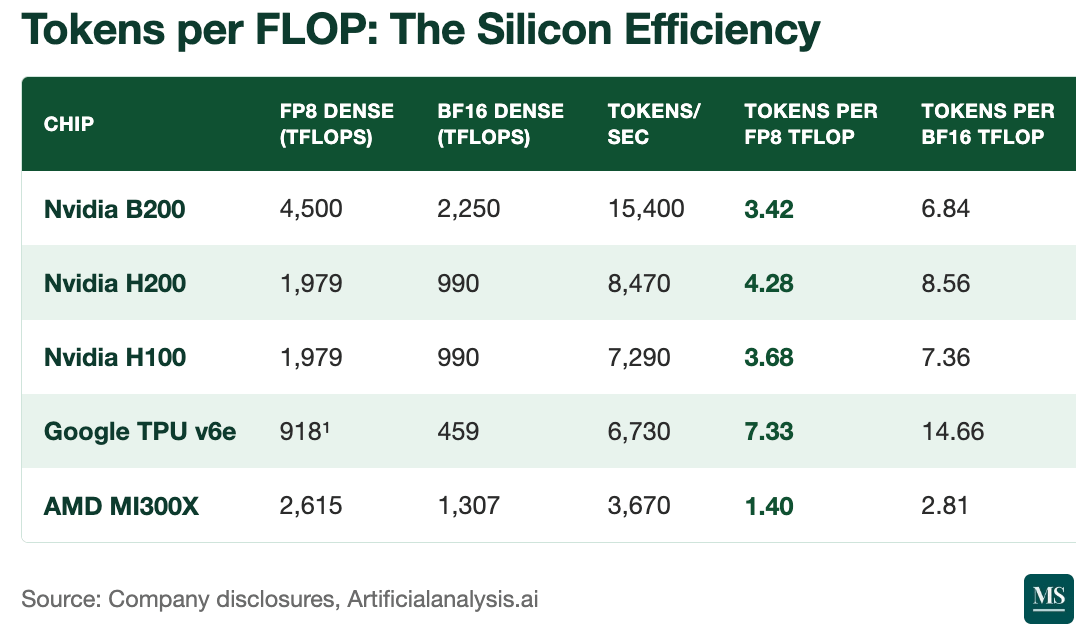

Artificial Analysis benchmarked open source Llama models across hardware. The results below are clear: Google's TPUs squeeze roughly 2x more tokens out of each TFLOP than any Nvidia chip.

Your Margin Is My Opportunity

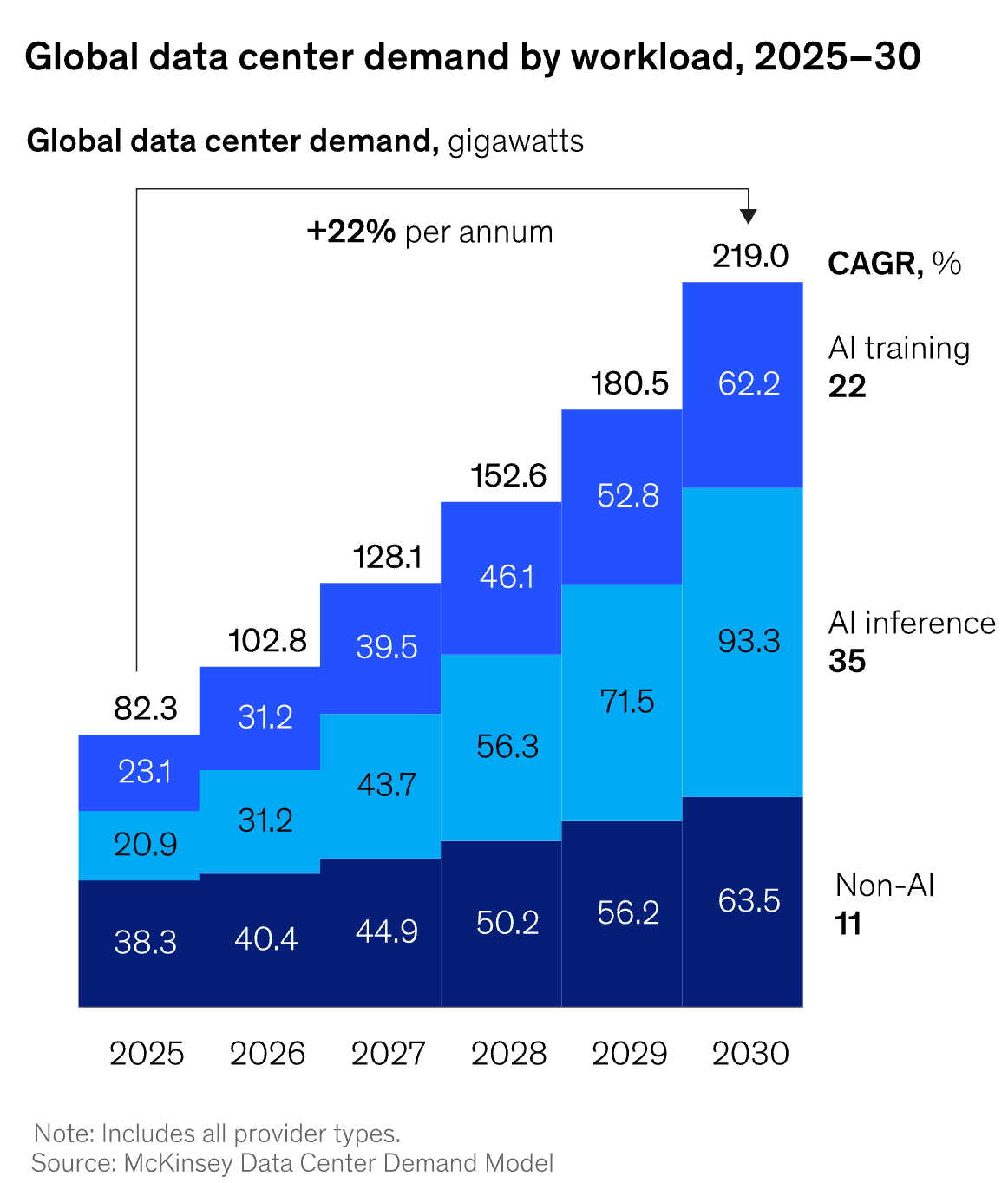

With AI going mainstream, the nature of AI compute is changing. Inference is starting to take a larger component of overall compute. Inference workloads are predictable and repetitive: exactly what custom chips are built for. Projections show that just the inference demand is the fastest growing segment at a 35% CAGR and will need 90GW of data center by 2030.

The catch with ASICs is that they are expensive to build. A leading-edge custom chip costs $500M+ in design, IP licensing, and tape-outs before a single unit ships. The math only works at scale. You need enough deployment volume that the per-chip savings outrun the upfront design cost.

Every hyperscaler has now crossed that threshold and is building their own chips.

Google has been at it the longest, and its TPUs are the most mature ASICs in production. Amazon is not far behind with Trainium and Inferentia, which we believe will boost AWS returns in the coming years. Meta is the newest entrant: its MTIA chips already run recommendation inference internally, and in February it signed a multibillion-dollar deal to lease Google’s TPUs, with talks underway to install them in Meta’s own data centers from 2027.

The race to serve models at the lowest cost

In our view, companies are currently in the token-maxxing era. Every employee, whether they need it or not, has access to frontier models with a nearly unlimited AI budget.

This will not last, for two reasons.

First, the C-suite is starting to demand ROI for the spend. Uber burned through its entire 2026 AI budget in four months on coding tools, and its COO now admits it is very hard to draw a line between token consumption and useful product output. Microsoft reportedly canceled most of its direct Claude Code licenses this month and moved engineers to GitHub Copilot.

Second, not every task needs a frontier model. Writing an email response or updating a deck does not require Claude Fable 5. An open source model can do the same work at a tenth of the cost or less, and as open models get smarter, the share of workloads running on them will keep expanding.

Note that this does not mean AI spend shrinks. Usage will keep exploding while the price per token collapses, so the pie grows even as every workload gets cost-optimized. What it means is that serving intelligence becomes a race to the lowest cost per token, the same way Japanese carmakers won the US market by delivering most of the performance at a much better price.

If that is the race, hyperscalers have no option but ASICs.

Investing in Accelerating ASIC Adoption

The custom ASIC market is projected to grow from 8% of AI accelerators today to 19% by 2033, a $118 billion segment compounding at 27%. Given how fast the open source models are improving, we believe this projection might be understated.

We have identified 5 companies that sit directly in this flow, and we are backing them with ~20% of the MS portfolio.