Deep Dive: MKS Inc ($MKSI)

Picks and shovels of picks and shovels

Usually, our approach at Market Sentiment for finding bottlenecks is going top-down — which simply means is we follow the capex trail to identify where the capital is flowing and which companies and industries stand to benefit. For example, here is a rough breakdown of Amazon will spend its $200B capex this year.

But one downside is that you will miss on relatively smaller companies whose deals won’t be big enough to show up in either 10K or news. To overcome this, you must do bottom up research where you go one by one to identify the common supplier.

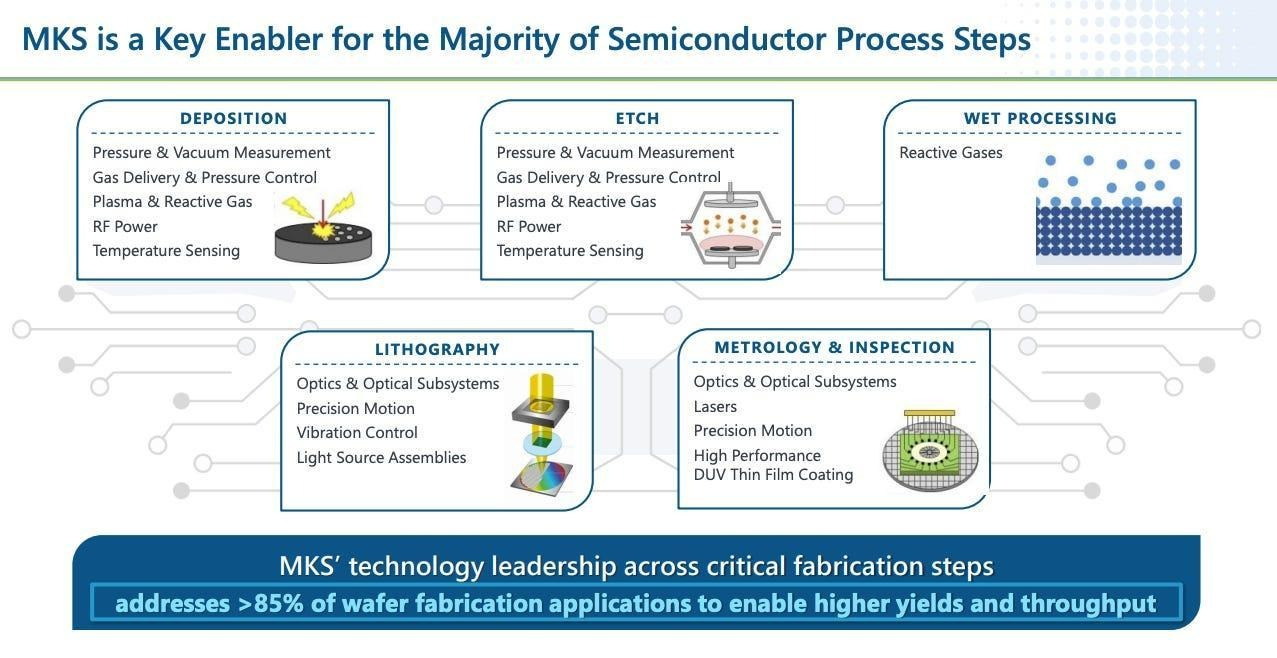

That’s exactly what we did to identify MKS Inc. MKS products are present in 85% of all semiconductor production tools worldwide. Nearly every step in the wafer fabrication process has an MKS component inside it and as far as we can tell, we are the first to cover this company in depth.

Market Sentiment delivers data-backed, actionable insights for long-term investors. Join 44,000 other investors to make sure you don’t miss our next briefing.

What does MKS do?

When TSMC builds a chip at its 3-nanometre node, the wafer passes through hundreds of process steps. Etching, deposition, lithography, inspection, cleaning. Each step requires a tool, and those tools come from equipment companies you may have heard of: Applied Materials, Lam Research, KLA, Tokyo Electron, ASML. These are the companies that collectively dominate wafer fab equipment spending, an industry worth roughly $133B in 2025.

But here is the thing. Those tools don’t work without subsystems. An etching chamber needs to maintain exact vacuum pressure, or the plasma that carves nanometre-scale features into silicon will behave unpredictably. That vacuum pressure is measured by an MKS gauge. The reactive gases that feed the plasma need to be delivered at precisely controlled flow rates, measured in nanolitres per minute. Those flows are controlled by an MKS mass flow controller. The RF energy that ignites the plasma in the first place is delivered by an MKS power supply.

If any of these are off by fractions of a percent, the wafer is ruined. At 3 nanometres, the margin for error is effectively zero.

MKS sells these subsystems to the equipment makers, who integrate them into finished tools and sell those tools to fabs like TSMC, Samsung, and Intel. MKS doesn’t sell to the fabs directly (for the semiconductor business). It sells to the companies that sell to the fabs.

It is, quite literally, the picks and shovels supplier to the picks and shovels makers.

MKS’s moat is exceptionally strong

The qualification cycles for semiconductor subsystems are measured in years. An equipment maker like Applied Materials doesn’t switch vacuum gauge suppliers because someone quotes a lower price. The gauge has been validated through months of process qualification at the end customer’s fab. The data, the documentation, the process recipes all reference that specific component. Changing it means requalifying the entire process. Millions of dollars. Months of engineering time. And most importantly, potential yield risk.

This creates an extraordinary moat. Not because MKS has patents (though it does have many), but because switching costs are so high that once you’re designed in, you stay designed in for the life of the tool platform. Often decades!

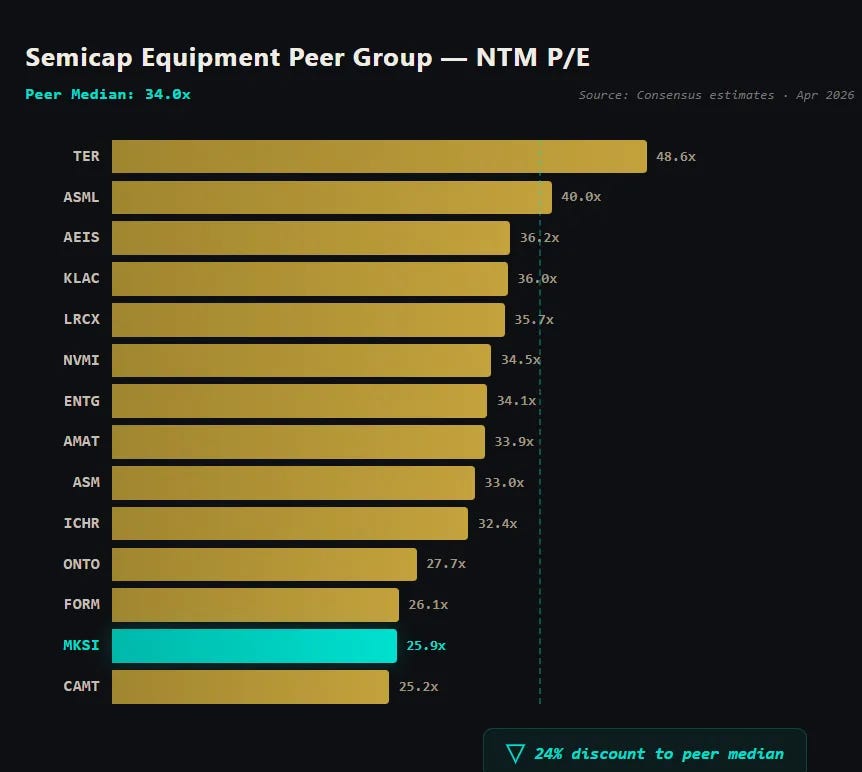

And yet, MKS trades at roughly 26x forward earnings, the cheapest forward P/E in the entire semiconductor equipment peer group (median forward multiple of ~34x).

One of the reason for the discount is the $4.4 billion debt load from an acquisition that, as we’ll argue, may turn out to be the smartest deal by any player in the sector. The market is mispricing MKS due to the debt-load, and the asset that it bought is structurally undervalued.

A far less visible layer of the Semiconductor world

There are really only five semiconductor equipment companies that matter. Applied Materials, ASML, Lam Research, Tokyo Electron, and KLA. Between them, they account for the vast majority of global wafer fab equipment spending.

But none of them build all their tools from scratch.

Below them sits a layer that is far more fragmented and far less visible. MKS, Advanced Energy, VAT Group, Inficon, Edwards, Brooks Automation. Each one commands a narrow, deeply technical niche. Vacuum. Power delivery. Gas flow. Measurement. Motion control.

The reason no single company spans all of these is that the physics is genuinely different in each domain. Building a mass flow controller that can meter corrosive gases at nanolitre-per-minute rates is a completely different engineering problem from building an RF power supply that delivers megahertz-frequency energy to a plasma chamber. The metallurgy is different. The sensor physics is different. The failure modes are different.

The equipment OEMs figured this out decades ago. If Applied Materials tried to build its own vacuum gauges, its own RF generators, its own laser systems, and its own gas delivery modules, it would need to maintain world-class R&D programs in half a dozen unrelated physics domains simultaneously. That would slow it down and dilute its focus on what it actually does best, which is integrating all of these subsystems into a finished tool and qualifying that tool at the customer’s fab.

So the OEMs outsource. And the subsystem suppliers specialize. And the result is an industry structure where five companies sit on top, visible to everyone, and a web of specialists sits underneath, visible to almost nobody, each one indispensable.

MKS, in our view is the broadest of those specialists. And that breadth is what makes it different from every other name in the layer below.

The Atotech Deal

In 2022, MKS acquired Atotech, a German company, for $4.4 billion. This was not a small deal for a company of MKS’s size. MKS’s EV was around $10 billion at the time of announcement of this deal. It loaded the balance sheet with debt, about $4.5 billion of it as of early 2026, which is why the stock traded at a persistent discount to its semiconductor equipment peers for years after the deal closed.

But the strategic logic was, in our opinion, genuinely brilliant. To understand that, we’ll need to understand what Atotech really does and how it integrates seamlessly with MKS.

Atotech is the global leader in advanced electroplating chemistry for PCBs and semiconductor packaging. Making a PCB requires plating copper onto its layers. That plating uses specialized chemistry, specific chemical formulations that have been tested and qualified for each manufacturer’s production process. Atotech makes that chemistry.

The business model works like this: MKS (through Atotech) sells specialized plating equipment to PCB manufacturers. That equipment runs on MKS’s proprietary chemistry. Once a PCB maker buys the equipment and qualifies the process, they are essentially locked into buying MKS chemicals for years. Management calls this a “high attach rate.” The industry term is more descriptive: it’s a razor-and-blade model.

Once the equipment is installed and qualified, the customer has no practical alternative but to keep buying MKS’s chemistry for years. The equipment sale is a one-time event. The chemistry revenue recurs for as long as the production line operates.

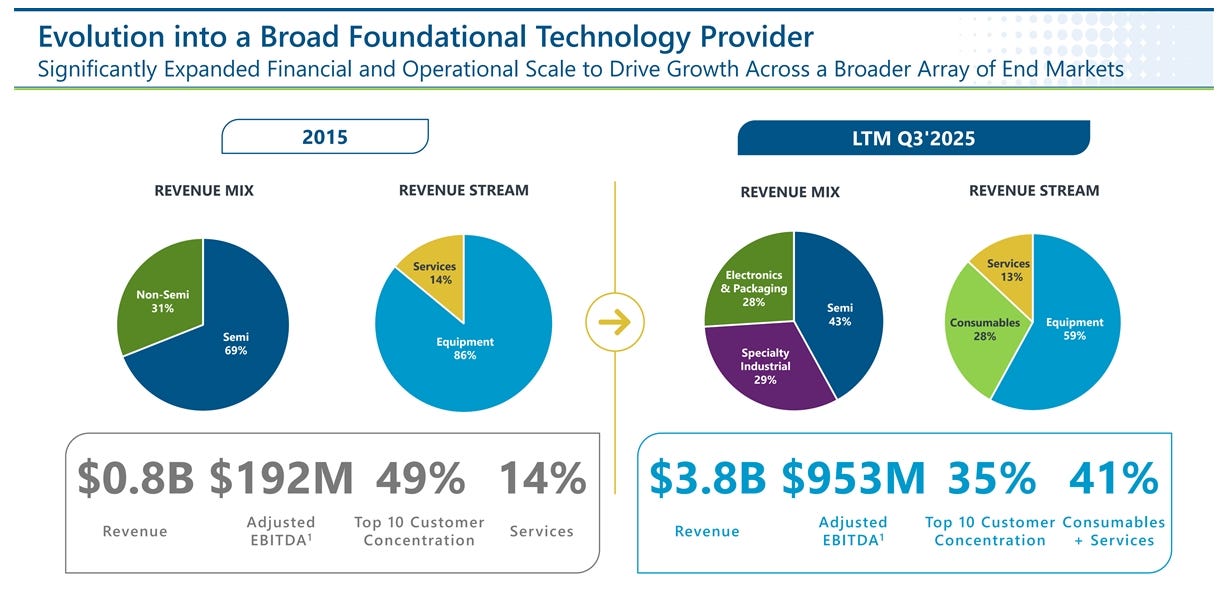

This is a fundamentally different business from MKS’s legacy semiconductor subsystem operation. Semiconductor subsystems are cyclical. When chipmakers cut capex, subsystem orders drop. But chemistry gets used up during production and needs to be constantly replenished. As long as the PCB factory is running, it needs chemistry. Management estimates that roughly 40% of MKS’s revenue now comes from consumables and services, chemistry that gets consumed in production and ongoing service contracts. This provides a layer of recurring revenue stability that the old MKS never had, which has also started to reflect in how markets are viewing the company.

Why the company is mispriced?

Now let’s dig into what has kept MKS’s stock at a persistent discount to its equipment peers (and why MKS is a strong buy at current prices):