Welcome to the latest Ideastorm. Market Sentiment curates the best ideas and distills them into actionable insights. Join 38,000+ others who receive curated financial research.

A quick note before we jump in — We recently introduced a lifetime membership to Market Sentiment. A few of you contacted us regarding the pricing structure, and we wanted to make it clear to all our readers that you will only be charged $399 once and not $399 annually.

You can change/upgrade your existing subscription.

Substack currently cannot do a lifetime membership. We manually stop the auto-renew for our lifetime subscribers and extend the subscription forever.

Actionable Insights

Even if you have long holding periods, there is no guarantee that a 100% stock portfolio will outperform a stock-bond blend.

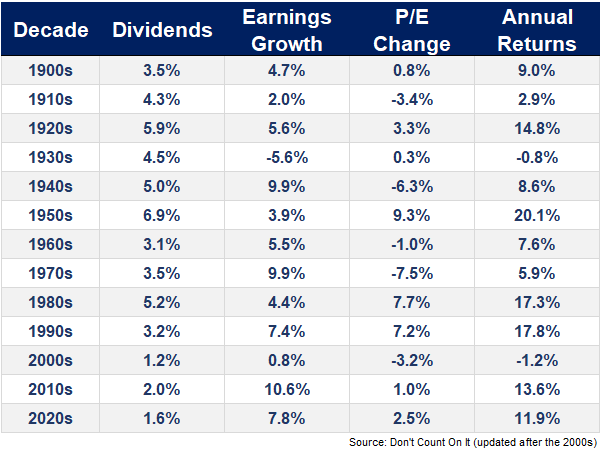

The majority of U.S. stock market returns since the end of the Global Financial Crisis were driven by earnings growth.

The higher your income, the more of it you need to allocate to your retirement (in % terms), and contrary to expectation, your highest spending is at midlife.

Factor investing is risky, but sticking to it is worth it in the long run.

The stock market was much more top-heavy in the 1950s than what we are experiencing now.

1. Stocks for the Long Run? Sometimes Yes, Sometimes No

Here is an interesting conundrum: There is an equity risk premium as stocks are considered more risky than T-Bills.

But if it's a near certainty that stocks will outperform in the long run (20+ years), why should there be a premium in the first place?

The answer partly lies in how far we go back with the backtest. Edward McQuarrie, Professor at Santa Carla University, backtested stock and bond performance in the U.S. dating back to 1793. He did this while improving the data coverage of underlying securities, reducing survivorship bias, and using market cap-weighted index for the analysis.

He found that over the 150 years from 1792 to 1942, stocks and bonds had similar performance. Sometimes stocks outperformed, sometimes bonds. But the beginning of World War II marked the worst bond bear market in U.S. history and skewed our perspectives on long-run returns.

Any 30-year rolling period from 1942 to 2019 had a 99% chance that stocks outperform bonds. But, pre-Civil War (1793 to 1862), the probability drops to zero!

The author argues that U.S. investors must accept that stocks will not always beat bonds, irrespective of the holding period.

US investors must accept that stocks will not always beat bonds, no matter the holding period.

However, presented in isolation, the new 19th-century US data could readily be dismissed as too old and obtained under far different macroeconomic conditions. The expanded international record provides crucial support, showing equity deficits and poor stock returns in recent times.

2. Fundamentals are driving the stock market returns

A common argument among value investors is that a majority of the stock market returns are driven by unsustainable valuations and increasing expectations. While this might be true for a few stocks, the overall market is growing based on fundamentals.

Ben Carlson has been continuously updating the expected stock market returns based on John Bogle’s simple formula:

Expected Stock Market Returns = Dividend Yield + Earnings Growth +/- the Change in P/E Ratio

While there was a significant multiple expansion in the 80’s and 90’s in the run-up to the dot-com bubble, the majority of market returns since the end of the Global Financial Crisis in 2008 have been driven by earnings growth (and not multiple expansion).

We recently dove into J.P. Morgan’s Guide to Retirement and found some fascinating insights.

If you are a non-smoker in excellent health, you must plan for at least 35 years in retirement.

If you are a 40-year-old couple with a $175K household income, you should have accumulated at least $500K in your retirement savings by now (to maintain an equivalent lifestyle in retirement).