QGV Framework for Investing

A smarter way to invest

Hi there —

This one’s a guest post by Rebound Capital. They have developed a proprietary framework for identifying and uncovering the best overlooked investment opportunities that are currently in a drawdown. Enjoy!

Rebound Investing is True Value Investing

Value investing is the pursuit of actively valuing different businesses and trying to buy them below their intrinsic value.

For example, if I offered to sell you a dollar note for 80 cents, would you take it? I am sure you would ask me if we can do the same with a million such notes! As value investors, our goal is simple: to buy a dollar for 80 cents or less. Value investors know that from time to time, the market will serve up a bargain. We need to be ready with our research and bet big when the opportunity comes.

Rebound Investing is not a new concept; it is a specialized approach within the world of value investing. While traditional value investing often focuses on finding cheap stocks across the board, our strategy is more targeted.

We specifically look for high-quality, growing companies that have experienced a significant price drop, which is often a result of market overreaction rather than a fundamental flaw in the business. We believe these temporary drawdowns create the most compelling bargains for value investors.

Key to Rebound Investing: Differentiate between Uncertainty and Risk

At Rebound Capital, our job is to differentiate between uncertainty and risk. Most investors believe a stock’s riskiness is defined by how much its price fluctuates. Even books on finance take the volatility of a stock as a proxy for the underlying business’s risk.

Our philosophy is that the risk underlying a business is directly proportional to the probability of a permanent loss of capital if we buy the stock. If we define risk as the probability of a permanent loss of capital, a company’s risk actually decreases as its price falls. This philosophy, that risk decreases as a company’s price falls, is the core of our value investing approach.

Of course, there are many nuances in this. The most important one is to ascertain whether the drawdown in the stock is due to an actual weakening of business fundamentals or if it is just the market’s sentiment that has taken a hit. The second important nuance is to value the company.

That’s where our QGV framework helps us identify the right opportunities.

Rebound Capital QGV Framework

How do we decide whether a stock that is in a major drawdown, implying large losses for its previous investors, is worth investing in? How do we judge its business model and future potential?

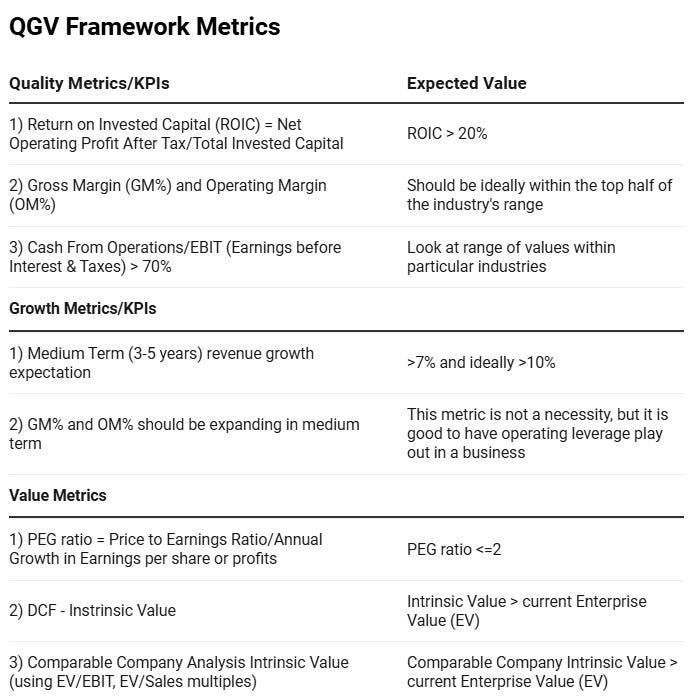

Our QGV framework helps us systematically analyze a stock’s potential by focusing on three key areas: Quality, Growth, and Value.

Quality: The Foundation

Quality metrics reveal the fundamental health and resilience of a company. A high-quality business is a fortress, and a price drop often presents an opportunity, not a warning sign.

Key metrics we use to assess a high-quality business are:

Return on invested capital (ROIC) - This metric measures how effectively a company is using the capital it has invested to generate profits. A high ROIC, ideally over 20% , indicates that the management team is a skilled capital allocator, which is a significant competitive advantage. We believe a company with a high and consistent ROIC is a sign of a strong business moat and a capable management team.

Profitability metrics like Gross Margin % and Operating Margin % vs industry benchmarks - These metrics, when compared to industry benchmarks, reveal a company’s pricing power and operational efficiency. A business with strong margins, that are at the high end of its industry, suggests it has a sustainable competitive advantage, as it can generate more profit from its sales than its competitors. We specifically look for businesses where both gross and operating profits are growing faster than revenue, which signals an improving market position and a widening moat.

Cash conversion ratios like Cash from Operations/Earnings before interest and taxes (CFO/EBIT) - This ratio measures how well a company’s profits translate into actual cash flow. A high cash conversion ratio, typically above 70%, indicates that the company is generating real cash from its operations, not just accounting profits. We prefer companies with strong cash conversion because it reduces the risk of relying on external financing.

Growth: The Future Potential

Growth metrics tell you if the company’s future is still bright. A deep drawdown can mask a business that is still expanding and taking market share, making it a potential bargain. Companies like Alphabet and ASML were both expected to grow revenue in double-digit % till 2030, but were still in a deep drawdown in early 2025.

At Rebound Capital, we generally look for businesses that have a minimum >7% expected growth in the medium term (3-5 years). We look beyond short-term growth hiccups. We have chosen 7% as a baseline growth rate because:

Beating Inflation and Protecting Purchasing Power: A primary goal of any long-term investment is to grow your wealth faster than inflation. Historically, an annual return of 5-7% has been considered a healthy rate, sufficient to outpace typical inflation rates. By targeting companies with a minimum 7% growth rate, we are establishing a baseline that aims not only to preserve but also to increase our members’ purchasing power over the medium term.

A Balance of Growth and Value: While some growth investors may target much higher growth rates, a 7% target helps us focus on companies with a more sustainable growth trajectory. We are not chasing speculative, high-flying stocks that may have high valuations based on unrealistic expectations. A 7% growth rate enables us to identify companies that are expanding their market share and have clear future potential, without the extreme volatility and risk often associated with businesses that are not yet profitable.

We also look for businesses where the gross profit and operating profit are increasing faster than the company’s revenue – which is usually a sign of improving market position for the underlying business.

Value: The Bargain Price

Value metrics help you determine if the stock’s price is a genuine bargain. A deep drawdown is not a buy signal on its own; it must be accompanied by a price that is compellingly cheap relative to the company’s fundamentals.

We try to look for companies trading at a fair valuation or trading below their intrinsic value (as we showed in the GOOG deep dive). While valuation is subjective, a quick discounted cash flow analysis or a comparable company analysis usually gives a good sense of its fair value.

We use the following metrics to assess a stock’s value:

PEG Ratio (Price to Earnings Ratio/Annual Growth in Earnings per share): We target companies with a PEG ratio of less than or equal to 2. The PEG ratio is a powerful tool because it factors in a company’s growth rate, providing a more comprehensive view of its valuation than the traditional P/E ratio alone. We are not too stringent with the PEG ratio (some firms use a PEG of 1) as we do not want to miss high growth opportunities (which can have high PEG ratios).

Discounted Cash Flow (DCF) Analysis: This method helps us estimate a company’s intrinsic value based on its projected future cash flows. By discounting these future cash flows back to their present value, we can determine what the company is truly worth today. We only invest if a stock’s price is below our estimated intrinsic value, as this provides a margin of safety and a significant upside potential.

Comparable Company Analysis: This approach involves comparing a company’s valuation multiples (such as EV/EBIT or EV/Sales) to those of its peers in the same industry. If a stock is trading at a lower multiple than its competitors while sharing similar or superior fundamentals, it may be an indicator that the stock is undervalued by the market and a potential bargain.

Our QGV framework is a disciplined, step-by-step process that allows us to find investment opportunities with a high probability of a strong rebound.

First, we identify a company with high Quality metrics, which signals a durable business model. Next, we confirm its long-term potential by looking for Growth rates that can deliver outsized returns. Finally, we analyze its current Value to ensure we are buying at a bargain price.

By combining all these factors, this comprehensive approach enables us to identify businesses that are in a temporary drawdown, rather than those experiencing permanent business issues.

Note that while quantitative metrics can help us screen for stocks, they are not hard rules, as some of these ratios can change very quickly. Hence, there is always a degree of art or subjectivity in shortlisting names.

Revealing the Rebound Watchlist

Our process for identifying rebound candidates is a systematic three-step approach: screening, shortlisting, and a final investment decision.

Here’s our full process and 30 companies with a Rebound Capital rating: