Deep Dive: SK Hynix

Capitalizing on AI-manufactured scarcity

With this report, we are initiating the first-ever single-company coverage at Market Sentiment. SK Hynix is the largest position in our Advanced Packaging portfolio and is perfectly positioned to capitalize on the AI Capex boom. Let’s dig in:

In 1999, when the Asian financial crisis hit South Korea hard, the government was desperate to streamline the economy and ordered a series of mergers. One of these was the shotgun wedding between Hyundai Electronics and LG Semicon. LG didn’t want to sell, and Hyundai didn’t want to buy, but the government forced the issue. This chipmaking business was unprofitable and debt-laden.

For what it’s worth, Hyundai had good reason not to buy. The company nearly went under due to debt during the dot-com bubble crash, and to prevent an overall collapse, the chipmaking business was spun off and renamed Hynix (a blend of Hyundai and Electronics).

By 2011, Hynix had been under the control of its creditors for over a decade. No company wanted to own Hynix. To keep a chip company alive, you don’t just buy it once; you have to pour billions into capital expenditure every single year just to keep the factories from becoming obsolete. Hynix was essentially a zombie company with seemingly no light at the end of the tunnel.

Enter SK group.

SK Group is South Korea’s second-largest conglomerate, specializing in semiconductors, energy, telecommunications, and pharmaceuticals. The Group’s chairman, Chey Tae-Won, said that the group needed a “new growth engine” because the domestic telecom and energy markets were saturated. Although this decision drew backlash from investors and analysts, SK bought a 21% stake in February 2012 for approximately 3.4 trillion won ($3.1 billion).

What happened next was a complete reversal of how Hynix had been run for the previous 10 years:

SK Group had massive trust in its newly acquired child. They readily opened their purse for a massive R&D expansion. The banks had previously starved Hynix of cash, and the company could only spend what it earned. SK Group immediately invested $3.5B in the first year, despite the chip market remaining depressed. This gave the company a head start on the next generation of technologies, while its competitors cut costs in a weak market.

With this investment, SK Hynix now had the best tools in the world. With the deep pockets of the SK group, the scrappy, survivalist culture of Hynix was transformed into that of innovation and tech leadership. This investment surge funded early research into HBMs, which is now helping the firm post record-breaking results.

Luck also played a part — just weeks after SK finalized the deal, Elpida Memory (a major Japanese competitor) declared bankruptcy. This cleared the field, leaving only three major players in DRAM: Samsung, Micron, and the newly reborn SK Hynix.

By the memory market upswing of 2017-2018, the company was making more profit in a quarter than the entire $3 billion purchase price SK had paid in 2012.

Market Sentiment dives deep into the bottlenecks of the AI world. Join 65,000 other investors to make sure you don’t miss our next briefing.

Business Overview

The company primarily makes DRAM (Dynamic Random Access Memory) and NAND memory chips (long-term storage). Traditionally, most clients for these products were smartphone and PC manufacturers, and the market was chugging along just fine.

Then AI changed everything — models required enormous amounts of memory to operate, and AI-generated images and videos required significant storage. With companies spending hundreds of billions in capex, the demand for DRAM and NAND skyrocketed, far outstripping the available supply. As a result, SKY Hynix’s revenue tripled from $22.8B in 2023 to $66.3B in 2025.

The company operates in two major segments:

DRAM (Dynamic Random Access Memory)

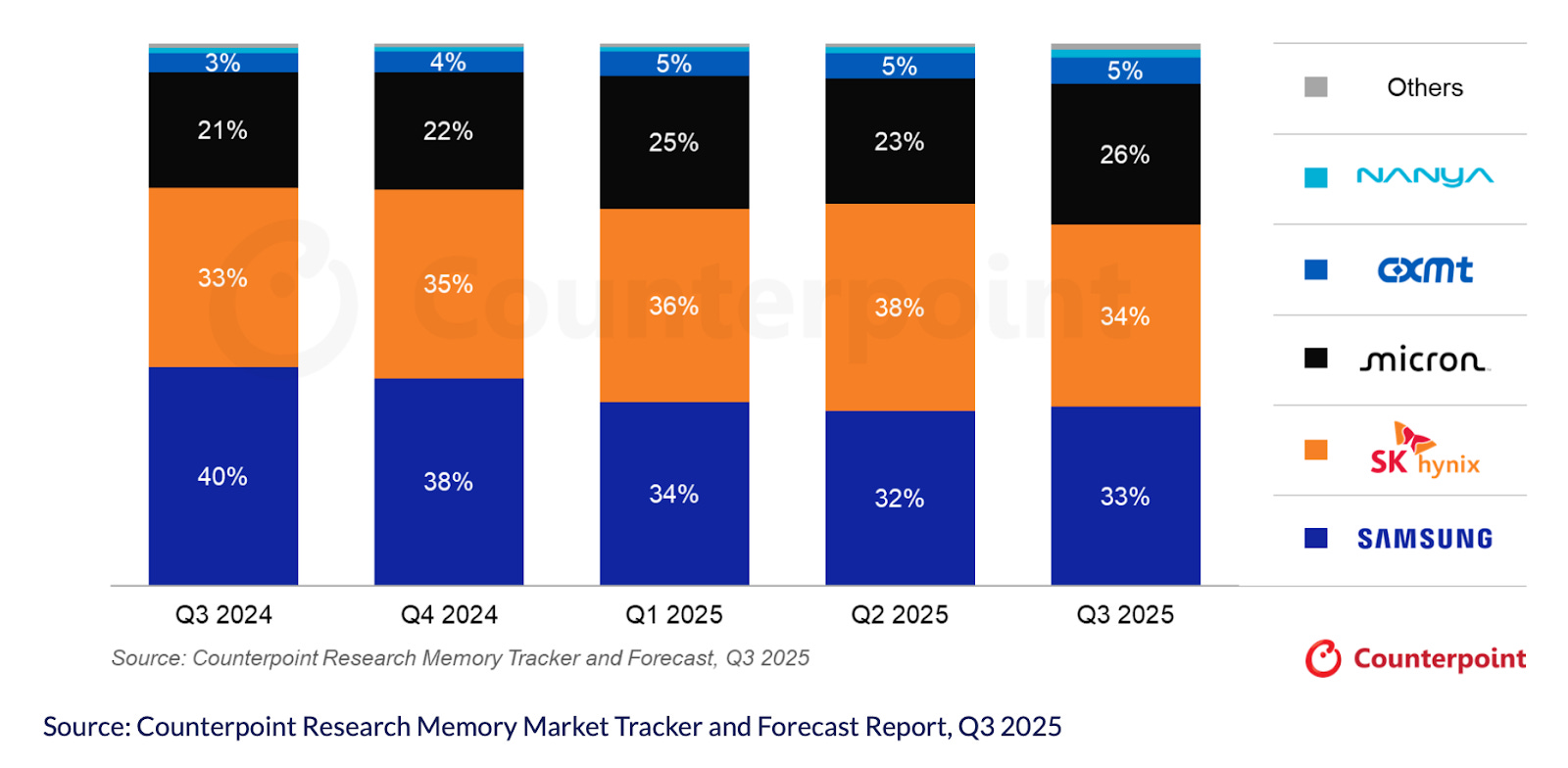

DRAM refers to the volatile, temporary memory used in servers, PCs, smartphones, and GPUs. In simple terms, DRAM is the memory where your device stores applications you are currently working on. Without it, the computer must search every file in permanent memory to retrieve it. If you've ever experienced lag when too many applications are open, it’s likely because DRAM was full and the computer was using slower, permanent storage. The segment accounts for 76% of the company's total revenue, and SK Hynix has a ~35% market share in the DRAM market.

The DRAM segment also contains the highly sought-after high-bandwidth memory (HBM). HBMs are created using advanced pacdeliver significant performance gains in memory speed, without which AI processors would sit idle most of the time waiting for data transmission. Given that HBM has emerged as a critical bottleneck for AI chips, the segment is projected to grow at a robust 40% CAGR over the next three years.

NAND Memory

NAND refers to the permanent, non-volatile storage that retains data without any power. This segment accounts for 23%s revenue.

Only five years ago, SK Hynix's NAND segment was widely viewed as a loss-making “secondary” business. The acquisition of Solidigm (a semiconductor subsidiary) for $9B from Intel in 2021 has helped turn around this segment. The company has strategically moved away from the volatile consumer SSD market to prioritize high-margin enterprise SSDs (eSSDs) for AI data centers. This pivot towards specialized, high-capacity storage has further boosted the company’s profitability and overall margins.

Sandisk ($SNDK), which has delivered 1500%+ returns to shareholders over the past 6 months, operates exclusively in this segment. SK Hynix has substantial exposure to the segment and is an alternative to Sandisk at a much more attractive valuation.

Capitalizing on AI-manufactured scarcity

Being positioned perfectly during the perfect storm of supply constraints and surging demand meant the stock has quadrupled over the last year, after being flat for the previous 5 years.

Based on our valuation model and industry projections, we believe there is significant upside still left in the stock.

Let’s dig in: