Deep Dive: Texas Pacific Land Corp ($TPL)

Right place, right time

This post is in partnership with Rebound Capital. When they covered the company back in October 2026, they had issued a hold rating with the following justification:

Given that we have no insight into how oil and gas pricing will behave over the next few years, and with the potential for TPL to pivot strategically into AI data centers, we will issue a Hold rating for now.

But given that both of these situations have materially changed in the past few months, it’s worth taking another look at the company. But before we jump in, settle an argument for us:

You probably have that one friend who owns a couple of rental properties and never stops raving about how effortless the passive income is.

Now, imagine owning almost a million acres of land. That’s exactly what Texas Pacific Land Corp (TPL) has — They have over 880,000 acres of land in Texas.

The company has a fascinating history. In 1871, the Texas and Pacific Railway Company began building a transcontinental railroad from Texas to California, and the states agreed to grant land for every mile of rail built. While the company was never able to complete the railroad and went bankrupt, it had built 972 miles of track, entitling it to 3.5 million acres of land in Texas. In 1888, this land was placed in a trust (Texas Pacific Land Trust) for the benefit of bondholders who had invested in the railroad.

The trust sold the land bit by bit to repay the bondholders and began leasing land to oil and gas producers in the 1920s. This was smart as there is no operational or capex risk for the company, and they just take a small cut from the oil produced on their land.

The stock basically went nowhere for 35 years after IPO(from 1985 to 2010), as the company’s main source of revenue was selling small parcels of land and royalties from leasing land to oil and gas companies.

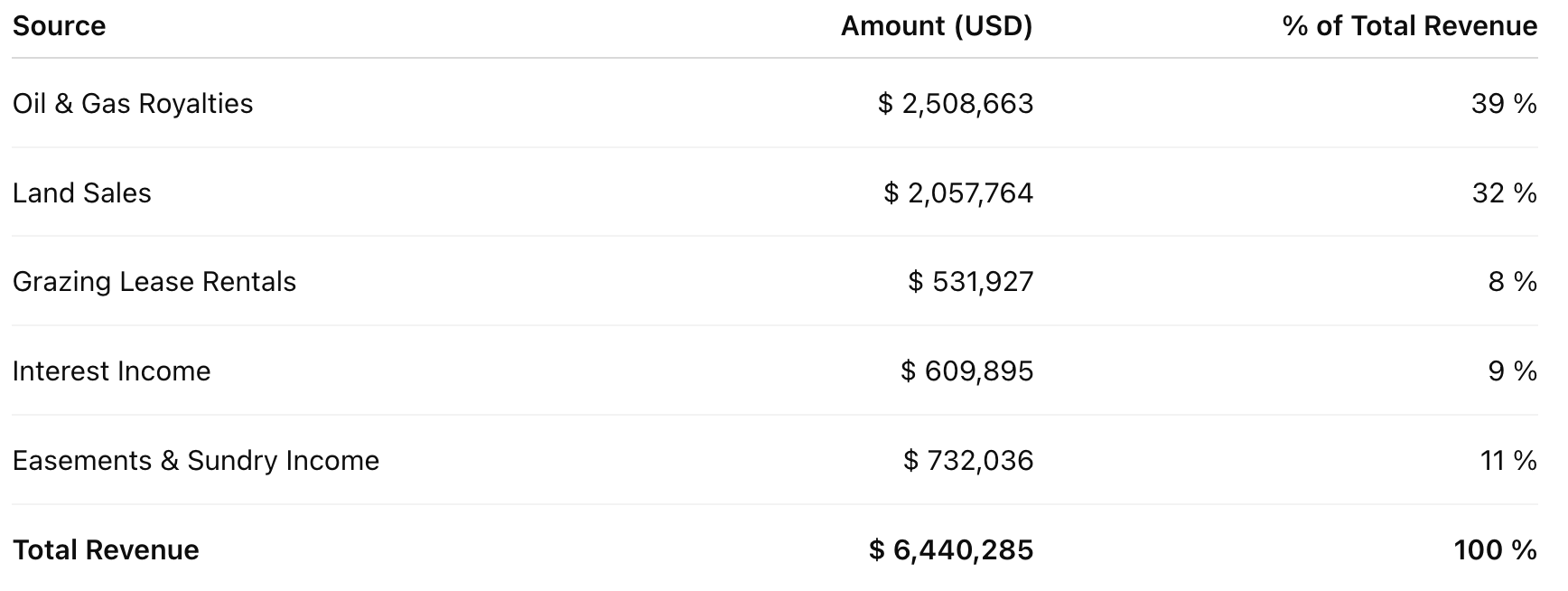

Digging into the 1995 10-K, we find that the company made a total of only $6.5 million, of which 32% came from selling the land. Obviously, this was never a sustainable source of revenue.

Everything changed around 2010 when oil and gas operators developed an advanced drilling technique that enabled them to drill sideways instead of just drilling down. By pumping water and sand through these long horizontal wells, they could crack the rock open and release far more oil than before which made it profitable to drill in TPL’s land.

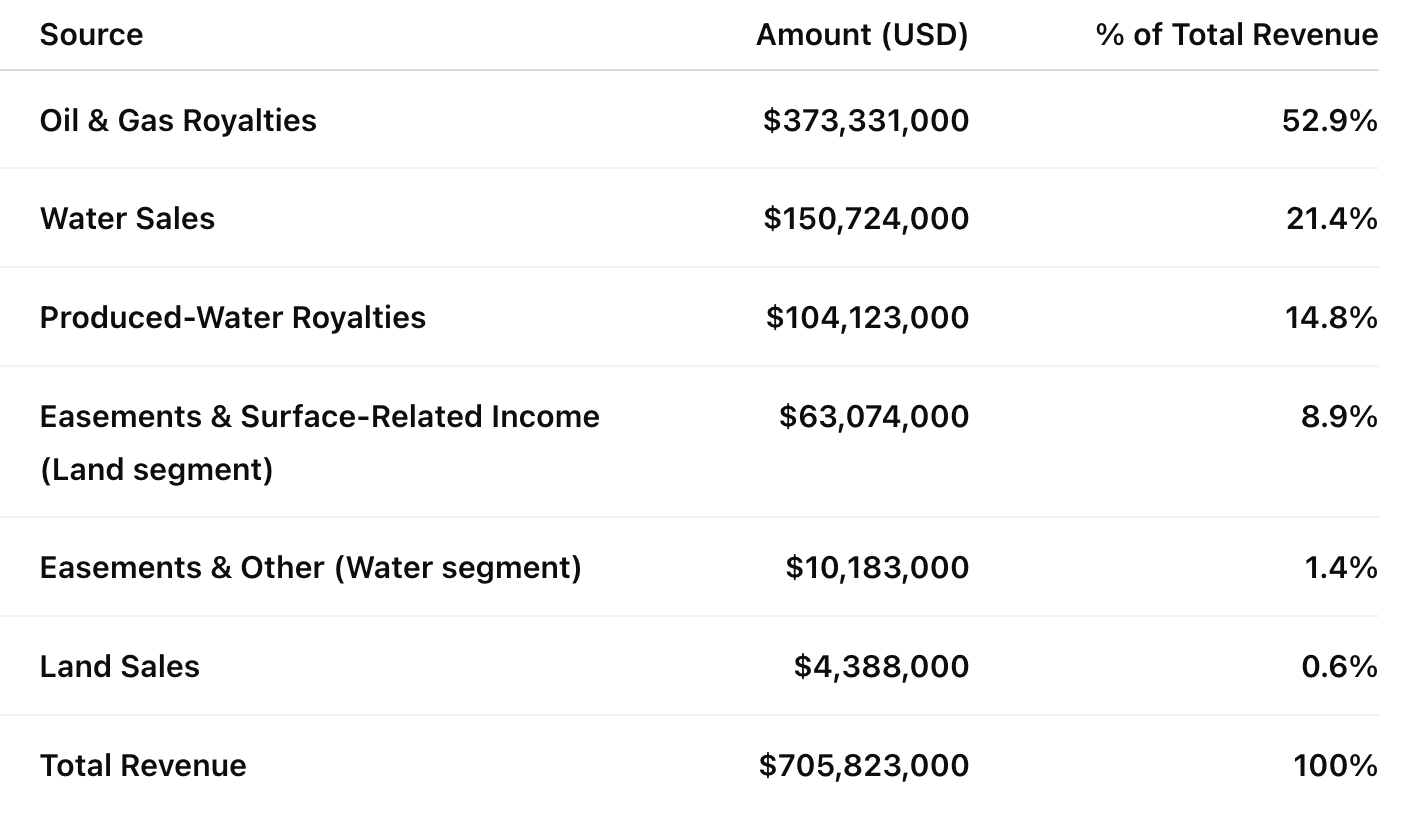

TPL’s revenue exploded. From only $2.5M in oil and gas royalties in 1995, it grew to $373M by 2024. TPL also diversified its revenue stream by selling & recycling water to oil and gas companies, as the new technique was water-intensive.

This is precisely why owning a perpetual asset is beneficial.

TPL had to wait almost 90 years since the first well was drilled for the technology to develop enough to make drilling on their land economical.

But once it did, the returns were incredible. TPL has now generated a 100x return over the last 15 years. (That’s 4x return of Apple!)

Market Sentiment dives deep into the bottlenecks of the AI world. Join 64,000 other investors to make sure you don’t miss our next briefing.

The cyclical nature of TPL

TPL is directly exposed to the price of commodities as it gets royalty on each barrel of oil produced on its land. This means that producers have less incentive to drill as oil prices fall. For example, in its Q2 2025 results, TPL reported a 21% drop in its royalty payouts per barrel , which led to an earnings miss in both revenue and EPS.

Since the company is trading a premium valuation, any earnings miss cause brutal drawdowns (as we can see below — 2015 Crude dropped from $100 to $30, 2020 Crude briefly went negative, 2023 post Ukraine spike).

Yet, the latest drawdown in 2025 (down ~50%) was predominantly the AI hype cooling off. The stock tripled in 2024 (up 233%) due to the expectation that TPL would get into AI data centers. Investors expected it to be a shoe-in, as the company already hosts some Bitcoin miners and has access to natural gas for energy and fresh water for cooling. Surprisingly no deal materialized for the company till end of 2025!

But two developments over the past few months have materially strengthened the bull case for TPL.

Let’s dig in: