Future Proof

Investing based on your priorities

Welcome to the 300+ investing enthusiasts who have joined us since last Sunday. Join 25,616 smart investors and traders by subscribing here. It’s totally free :)

Check out our - Best Articles | Twitter | Reddit | Discord

It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so. - Mark Twain

The investing questions that interest me the most are the ones I’m personally worried about. I explored the importance of a good start because I was perturbed by market volatility as a beginner and I wanted to see how someone who just started investing could set themselves up for success. But of late, there’s a question that’s been bothering me a lot more: What weaknesses in my portfolio am I not aware of?

The biggest disasters in investing are the consequences of failing to foresee the unexpected - From the Dot-com Bubble crash, to the failure of banks to see the housing bubble explode. Comfort in the wisdom of the crowds can trip you up. And one thing that the crowd (including me) repeats over and over is “In the long term, the market always wins.”

In the long term, that’s true. But returns become real only when you sell. Sometimes, you don’t have control over that. The biggest blow could be…

Selling when you don’t want to

Before we jump in,

As you know, I am not a big fan of clickbaity titles. You will never see one from Market Sentiment and that’s what I like about The Daily Upside*. They provide calm and collected insights without fear-mongering. It’s a completely free, high-quality newsletter, it’s all you need to make sense of the economy in 2022. Sign up at no cost here*.

*This is sponsored content

Now, back to it: Even though the market has very good returns over a long period of time, the returns seen by investors might be very different. The major reason for this is that investors sell when they don’t want to. It could be because of panic induced by market crashes, a health emergency, a personal crisis, or any of several reasons. Nassim Taleb calls them “uncle points”, a situation in which your arm is bent behind your back and you scream out “Uncle!”

Or it could even be that you are in a transition period such as retirement, or quitting a job to pursue other options. The worst possible scenario is when there’s a golden buying opportunity in the market because of a crash or a bear market, and you simultaneously need to liquidate your investments due to a lack of funds. How can we protect against such a possibility?

The most obvious solution is to have an emergency fund for such scenarios, but another option is to get

Insurance against the market

Unless you were living under a rock for the last 10 years, you’ve watched “The Big Short” or at least heard of it. The movie focused on the housing market crash and how a handful of people became incredibly rich because they spotted an opportunity. But at the heart of the whole story is the Credit Default Swap - An instrument that let them take advantage of a rare event.

Simply put, the swaps were derivatives that acted like insurance against an event that had a very low chance of happening. Hedge funds use similar methods for a different reason: They buy common stock to balance against the derivatives they trade-in.1 The methods to do these are quite complicated for retail investors to use - but a simpler alternative is to buy index put options as you keep investing into the S&P500, and if the market crashed, the puts would increase in value, and you would be insured. Sounds good right?

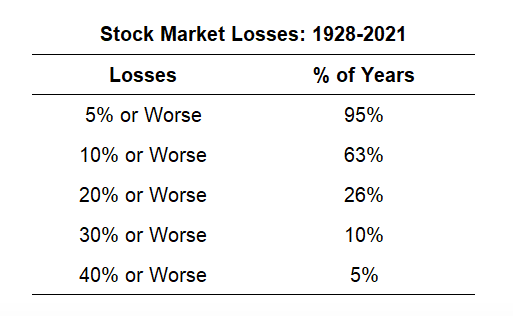

There’s a caveat to this approach: Disasters don’t happen that often. The premiums you pay on the puts might eat into your portfolio’s returns in the long run - Kind of like paying high amounts for car insurance in a safe town and running out of money for gas. As shown below, a 30% crash happens only 10% of the time.

AQR Capital researched this topic further and found that buying puts works over the short term, but over the long term it's not optimal. At the end of the day, your insurance shouldn’t become your investment strategy, and being a black swan hunter isn’t worth it.2 But if you are close to retirement, or you have a short investment horizon, buying puts is one way of hedging against loss of capital.

But is there a simpler way of doing the same thing?

What you can control

Despite the great track record that the stock market has had over the last few decades - I hate to admit this - luck plays a large role. For example, if you consider three people who had invested in the markets every year starting in three different years, this is how the returns would have been in the first ten years:

You cannot control which year you are born in, or what will happen in the next decade. But if you are nearing retirement or saving up for a short-term goal, it’s more important to preserve capital than to reach for gains. Is there a reliable way to do this? It turns out that the simplest way to do this is to have a rebalanced portfolio - A portfolio where you maintain a fixed proportion of stocks and bonds by adjusting the balance every year or so.3

To see the advantage, let's consider two portfolios: an all-stocks portfolio and a portfolio that has 60% stocks and 40% bonds. Every year, I would invest 100 dollars into both portfolios, but in the case of the 60-40 portfolio, I would rebalance.4 Let's compare the lowest values that the cumulative returns can drop to:

In most cases, the minimum cumulative returns of the stocks-bonds portfolio are higher than that of the stocks portfolio. This means that when times are bad, or if there is a sudden market correction, the chances of losing your capital are much lesser with a mixed portfolio. This is especially important if you have a short-term goal or are nearing retirement, in which case your investments would dry up and it’s the allocation that becomes important.

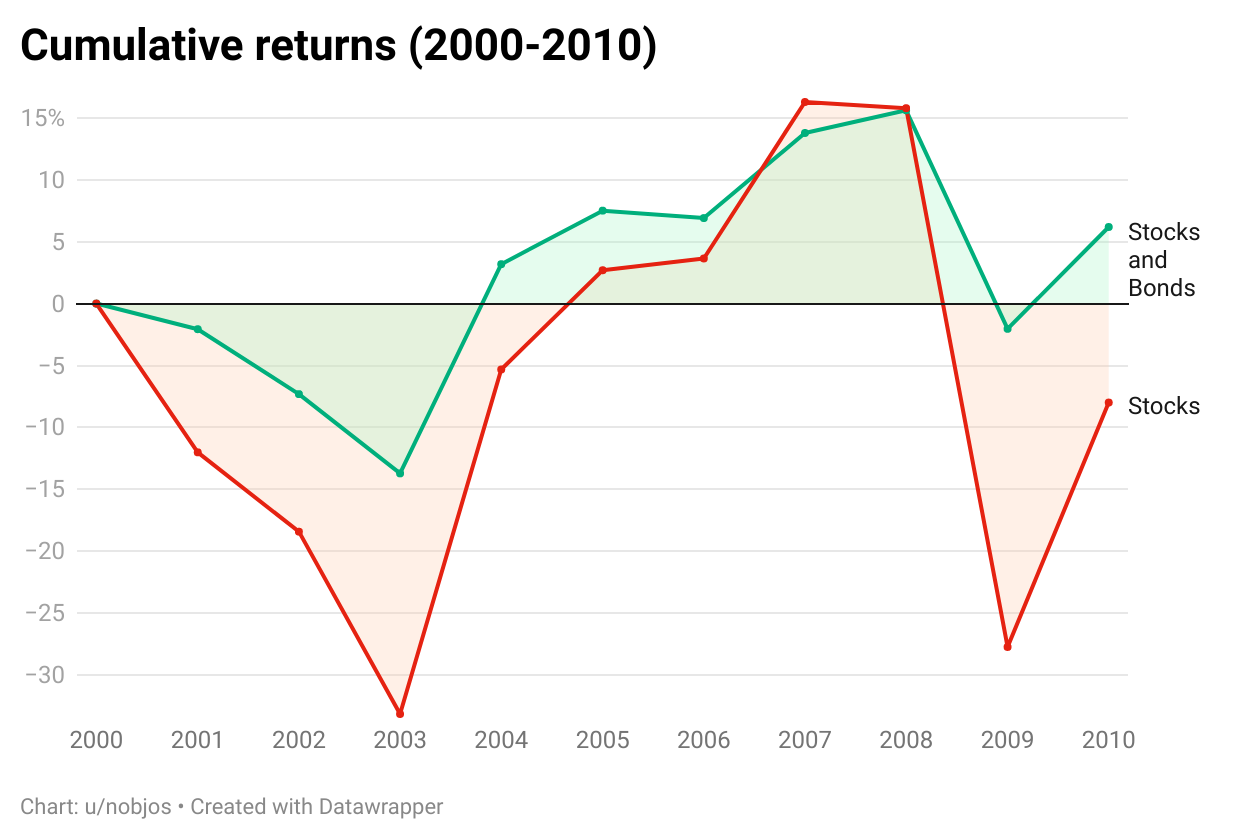

To drive home that point, let’s consider the worst starting point, the year 2000, and compare the cumulative returns.

Retiring in this decade without adequate protection would have been very stressful, and would have cut into future returns as well. But the rebalanced portfolio had positive returns 60% of the time, and even when the market is down, the losses are cut - If you had been forced to sell in 2008 for example, you would have lost 27% of an all-stocks portfolio, but only 3% if you had mixed in bonds!

Of course, the trade-off with a rebalanced portfolio is that returns would be lower over the long run, and if you have a longer investment horizon, you can hold lesser bonds in the mix. But you always have the freedom to change the proportion of stocks to bonds, and over shorter durations, the low returns are more than made up for by the security that a diversified portfolio provides. I have considered a 60-40 split here, but holding even 10% bonds can cut losses to a large extent.5

Many times, investing is seen as an exercise in getting the most returns possible. But thinking about your finances in a more holistic way can save you a lot of stress. With so much emphasis on reaching for the upside, we forget that the downside is what we need to protect against first. And there are a lot of things that you can actually foresee and prepare for, outside of your investment portfolio:

What major financial requirements might arise in the next 5-10 years? (College for children, buying a house, etc.)

What disasters can I protect against by buying insurance? (Fire, disease, accidents, death, etc.)

Can I structure my finances better?6

What’s the worst that can happen? If I lose my job and the stock market crashes and the economy goes down, do I have an emergency fund that can pull me through?

Planning for these makes it less likely that you will disrupt your investment portfolio in bad times, and an uninterrupted portfolio is the key to larger gains.

And last, but not least, you can prioritize uniformity and safety of outcomes as much as magnitude by diversifying. A little more predictability and protection might be the greatest thing you can ask for especially if you’re starting to think of retirement. Invest according to your priorities instead of a single number, and your future self will thank you.

Do you have a better way of balancing risk and returns? How do you protect against downturns? Let me know in the comments or jump into our Discord to continue the discussion.

A lot of research went into this article and if you enjoyed it, please do me the huge favor of simply liking and sharing it with one other person who you think would enjoy this article! Thank you.

Disclaimer: I am not a financial advisor. Please do your own research before investing.

P.S - if you are interested in any kind of partnership, sponsorship, or bespoke consulting services feel free to reach out at marketsentiment.live@gmail.com.

Footnotes

Michael Burry and Co. were not the first to do this. Legendary investor Ed Thorp would be long on common stocks and short on warrants to balance the price changes, and this was a precursor to the Black-Scholes formula that was used extensively by hedge funds later on.

Check out Moontower Meta’s article on people who saw the housing bubble and chose to not short it.

You can add other assets to the mix too. Check out my article Red Pill, Blue Pill which dives into many other possibilities.

In some years, this means selling one portfolio to add to the other. This would bring in tax implications, which I have ignored here.

The data for this analysis has been taken from Aswath Damodaran’s website. The bonds considered here are US T-bonds.

Once again, a great article very much needed during these uncertain times. I continue to be very grateful for your time, research and thoughtful commentary. I know that you don't charge for this exceptional service, so I would love to repay your kindness if you ever find yourself in the Riviera Maya, Mexico, by inviting you to sail with us on our beautiful turquoise waters