Welcome to the latest weekly Ideastorm. Market Sentiment curates the best ideas from thousands of research sources and distills them into weekly actionable insights.

If you are new here or someone forwarded this to you, join 35,000+ others who receive curated financial research.

Actionable Insights

There is a negative relationship between consumer sentiment and subsequent stock returns. (particularly interesting given the extreme fear in the market)

While past performance could predict future outperformance in mutual funds in the 80s and 90s, the latest research suggests that this alpha is vanishing.

Unsurprisingly, the latest SPIVA report highlights that 92% of large-cap mutual funds have underperformed the S&P 500 over the past 15 years.

Investing in “sin” stocks generated a Fama-French 6-factor alpha of 4%.

Companies having wide moats continue to outperform the market and generate excess shareholder returns.

1. Relationship between Consumer Sentiment and Stock Returns

Kenneth L. Fisher and Meir Statman — open access

Guide to the markets — JP Morgan

JP Morgan released a report that highlighted the effectiveness of using consumer sentiment for investing – On average, the S&P 500 returned only 4% in the next 12 months if you invested when the consumer sentiment was at its peak, whereas if you invested when the consumer sentiment was at its lowest, over the next 12 months, your average return would have been 24.9%! A 6x return increase just by investing when everyone else was skeptical.

But, the above analysis suffers from classic hindsight bias – we cannot know in advance if the consumer sentiment we see today is at a new peak or an all-time low.

Kenneth Fisher was one of the first investors to find the edge using consumer confidence & investor sentiment. He found a negative and statistically significant relationship between investors' sentiment and subsequent stock returns. But, he highlighted the shortcomings of using it for asset allocation (emphasis added).

The negative relationship between consumer confidence and subsequent stock returns is useful to investors even if it is too weak for robust tactical asset allocation.

The fact that low levels of consumer confidence predict high rather than low subsequent stock returns should reassure investors that consumer confidence and stock returns do not follow each other in an endless downward spiral.

Indeed, when people lose confidence as consumers, they should regain it as investors. – Kenneth Fisher

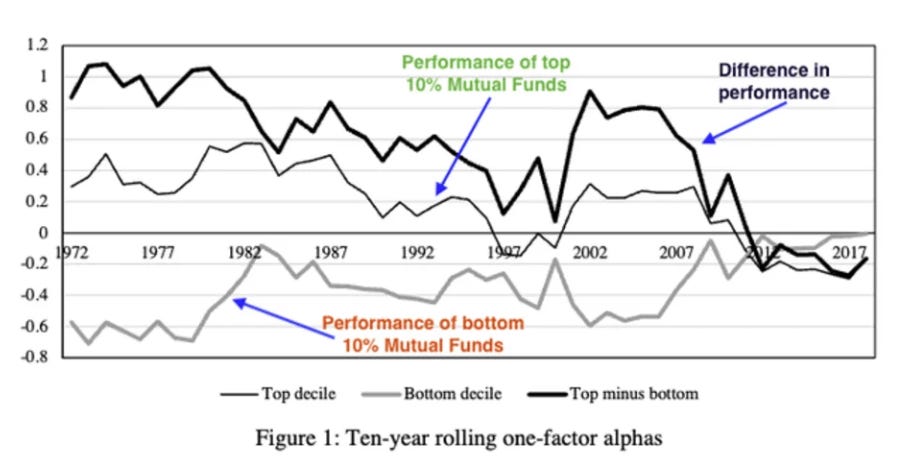

2. Can past performance predict the future outperformance of Mutual Funds?

Mark M. Carhart (1997) — open access

James J. Choi & Kevin Zhao (2018) — open access

Mark Carhart published his seminal study on this in '97 and found that past-year performance positively predicted the U.S. equity mutual funds’ future performance. The top 10% of the funds from the previous year outperformed the bottom 10% by 0.67% per month! (1963 - 1993).

The outperformance was mainly attributed to individual stock momentum. Momentum investing is well-proven, and funds with outperformance tend to hold high-momentum stocks. Fund managers rarely sell their winners, and the momentum effect carries over to the following year.

However, the study was done more than 25 years ago. When researchers at Yale University replicated the research done by Carhart and expanded it till 2018, they found that the best-performing mutual funds did not produce any alpha.

The difference in the 10-year rolling alpha of the top and bottom 10% mutual funds has declined over time, and after 2012, the bottom decile funds are performing marginally better.

3. Active vs Passive debate — Latest update from SPIVA

SPIVA report by S&P Global — open access

SPIVA Scorecard is considered the de facto scorekeeper for the active versus passive debate. Their methodology and data are immaculate, with adjustments for survivorship and calculating both equal and asset-weighted returns.

Here are the key takeaways from the latest report:

92% of large-cap mutual funds have underperformed the S&P 500 over the past 15 years.

A majority of large-cap managers outperformed the S&P 500 only thrice in the last 23 years.

In the first half of 2023, growth was king — 90% of large-cap value managers underperformed the index vs. only 13% of large-cap growth managers.

The S&P 500 growth index has posted its best first-half performance since 1998 (+21.2%), and last year's worst-performing sector (Communication Services: -22%) was among the best performers in H1’23 (+19%).

Most of the S&P 500 returns were driven by the index’s largest constituents.

The average return of the stocks in the S&P 500’s largest capitalization decile was more than double the average return of the next-best-performing decile.

Finally, over a 10+ year time horizon, there were no categories (small cap, mid-cap, value, etc.) where a majority of active managers outperformed.

4. Investing in sin stocks

Hamid Boustanifar, Patrick Schwarz — open access

Consider this controversial investment strategy: Investing in companies profiting from “sinful” services or products like tobacco, alcohol, and gambling. In 2020, over $15 trillion was invested with negative screening, excluding these companies from most funds, regardless of their appeal. Could this create a pricing imbalance that active investors could exploit?

To find out, the researchers analyzed the annual reports from 13,740 companies (1996 to 2021). Instead of using traditional industry classification to identify sinful companies, they used textual matching. If the company's annual report contained multiple mentions of words and phrases related to sin industries, they considered those companies in the final portfolios.

The portfolios were created using three methods

Value-weighted

Equal-weighted

Sin-weighted (in proportion to the exposure of the companies to sinful industries)

While (1) and (2) had no statistically significant outperformance, a sin-weighted portfolio (3) generated an annualized Fama-French 6-factor alpha of 4%1.

5. Do durable competitive advantages convert to shareholder value?

Srinidhi Kanuri & Robert W. McLeod — not open access

Warren Buffett was one of the first to popularize the concept of economic moats with his 2007 letter to Berkshire shareholders.

A truly great business must have an enduring “moat” that protects excellent returns on invested capital. The dynamics of capitalism guarantee that competitors will repeatedly assault any business “castle” that is earning high returns.

Therefore a formidable barrier such as a company’s being the low-cost producer (GEICO, Costco) or possessing a powerful world-wide brand (Coca-Cola, Gillette, American Express) is essential for sustained success.

Business history is filled with “Roman Candles,” companies whose moats proved illusory and were soon crossed.

Kanuri et al (Applied Economics) evaluated the performance of wide moat stocks from 2002 to 2014 using the Morningstar Direct stock database2.

All the wide moat stocks were used to create a portfolio starting in June 2002 and then updated every year based on the new list released by Morningstar. Both equal and market cap weighted indexes were formed for the portfolio backtest. The results were promising.

Wide moat stock portfolios were able to beat both the S&P 500 and Russell 3000 by a significant margin while having lower volatility. The risk-adjusted returns were also excellent, as seen from the Sharpe Ratio. They went one step further and evaluated the performance of the wide moat portfolio during the 2008 financial crisis and found similar trends. (emphasis by author)

Our results indicate that the Wide Moat portfolio performed better/lost less value than both S&P 500 and Russell 3000 indices during the 2007–2009 financial crisis as Wide Moat portfolios (both equal- and value-weighted) had better absolute and risk-adjusted returns over both the indices.

If you found this recently, the poll is closed. Here is the deep-dive:

Just a reminder that Market Sentiment is now fully reader-supported. A lot of work goes into these articles, and if you enjoyed this piece, please hit the like button and consider upgrading your subscription to access all our research and deep-dives.

Implies the strategy outperformed the benchmark index by 4% per year after accounting for all known risk factors (as per the Fama-French 6-factor model)

Morningstar is one of the key players providing data related to moats with their economic moat rating (classified stocks as Wide, Narrow, and No Moat). They look for companies that have generated a higher return on invested capital (than the cost of capital) for a long time.

I love these posts and I appreciate the way you explain each topic simply.