Leveraged ETFs

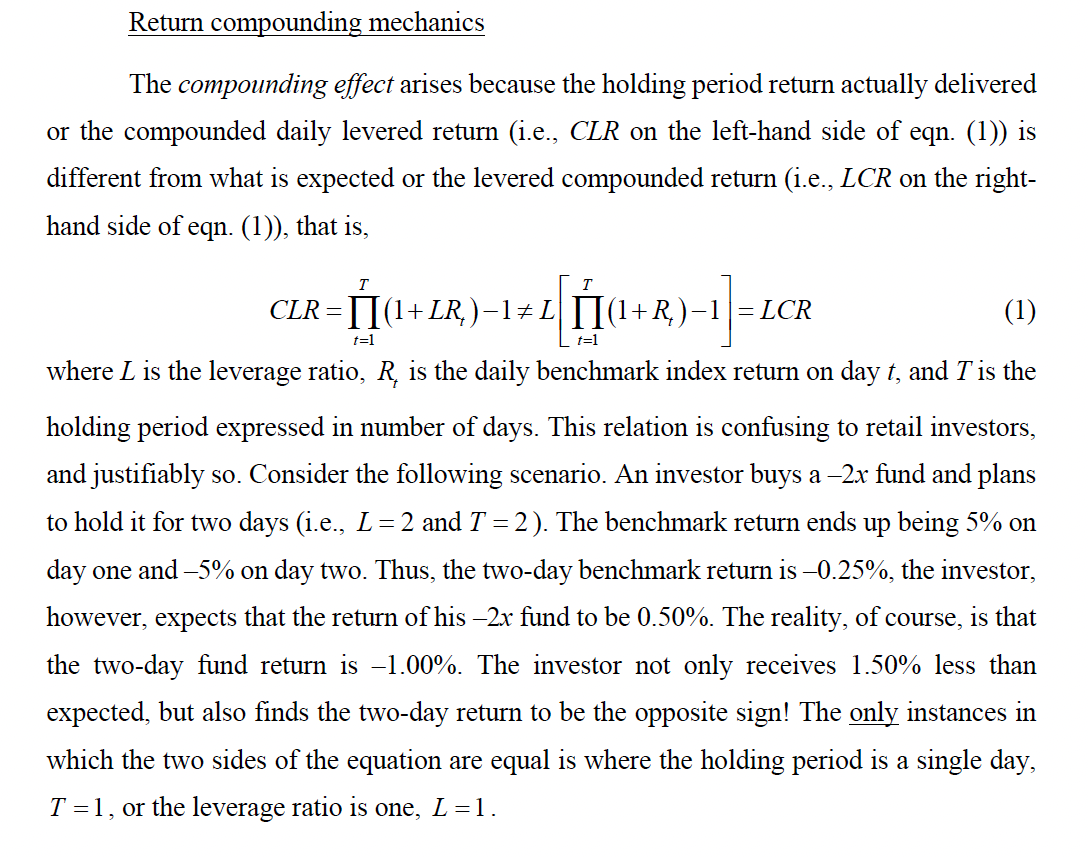

To lever or not to lever?

No paywall on this one. Share it with a friend :)

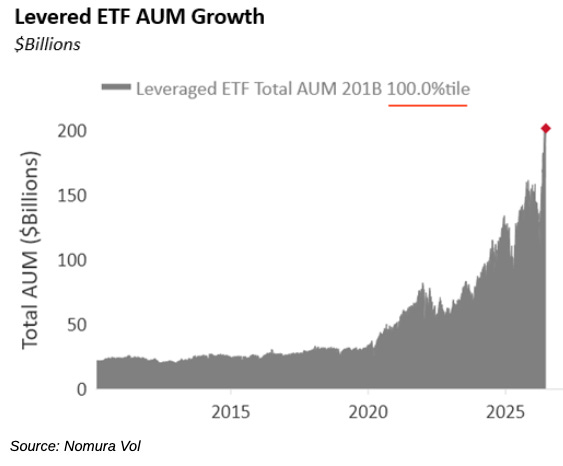

This one’s a bit different from our usual reports. I just saw an incredible stat from the Nomura research team, and it felt like a good time to revisit our research on Leveraged ETFs from two years ago.

Leveraged ETFs have grown nearly tenfold in the past decade. AUM now sits at an all-time high — this surge is a key driver of the rising volatility we are seeing in markets. The more concerning part is what sits underneath it. Most of this money is retail chasing performance in semiconductors. Over $50B in leveraged ETF AUM is now concentrated in semiconductor funds.

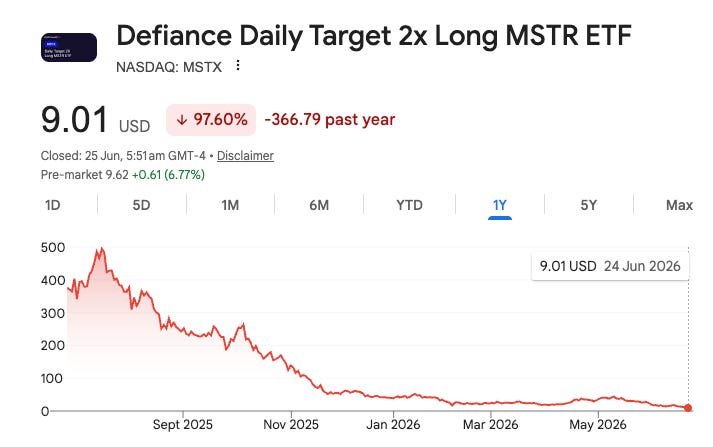

Investors buy 2X and 3X leveraged ETFs expecting 2X and 3X returns. It rarely plays out that way. The risk of capital loss runs far higher than intuition suggests. Here is what happened to the 2X-leveraged MicroStrategy ETF, a fund with over $1B in AUM.

Market Sentiment dives deep into the bottlenecks of the AI world. Join 46,000 other investors to make sure you don’t miss our next briefing.

To understand what’s going on, we have to first understand how leverage works in investing:

Let’s say that you had $10K in your brokerage account. You have a high-conviction stock you think is going up and want to invest more than $10K in it. You can take another $10K as a loan from your brokerage, staking your entire position as collateral.

Assume the stock went up 10% over the next month, and you exit the position.

This is the magic of leverage. You used a 2:1 leverage on your investment and doubled your return1

What’s important to realize is that this works the other way, too — If the stock went down 10% and you had to exit the position, the 2:1 leverage would literally double your losses.

Having a large amount of leverage is like driving a car with a dagger on the steering wheel pointed at your heart. If you do that, you will be a better driver. There will be fewer accidents but when they happen, they will be fatal - Warren Buffett

Understanding Leveraged ETFs

It’s vital to understand how leveraged ETFs work — class action lawsuits were filed (and later thrown out) because investors did not understand how they are structured.

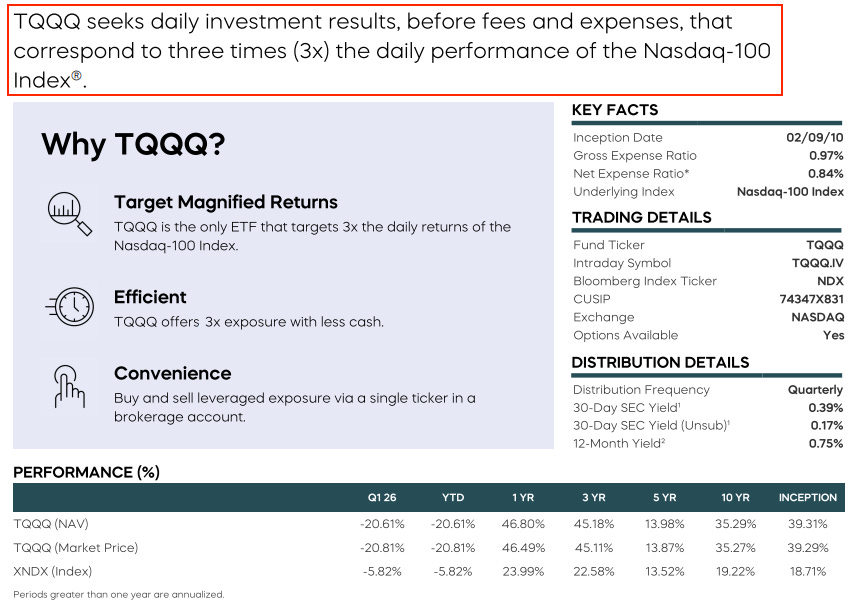

For example, let’s take a quick look at the TQQQ fact sheet:

The fund is only trying to 3x the daily return of QQQ and not the long-term return.

To understand how the index gains and index volatility affect the total return, consider this — Let’s say you invested $100 into QQQ and TQQQ. On day 1, the index went up 10%. On day 2, the index went down 10%.

Here’s how both funds would have performed2

Day 1:

Index (QQQ): 100 x (1 + 10%) = $110

3x Leveraged Index (TQQQ): 100 x (1 + 3 x 10%) = $130

Day 2:

Index (QQQ): 110 x (1 - 10%) = $99

3x Leveraged Index (TQQQ): 130 x (1 - 3 x 10%) = $91

Overall Return (after 2 days):

Index (QQQ): (99 - 100)/100 = -1%

3x Leveraged Index (TQQQ): (91 - 100)/100 = -9%

Intuitively, you would expect your 3x levered portfolio to go down only 3% when the underlying index went down 1%. But the leveraged ETF’s actual return (-9%) is much worse than the expected return (-3%).

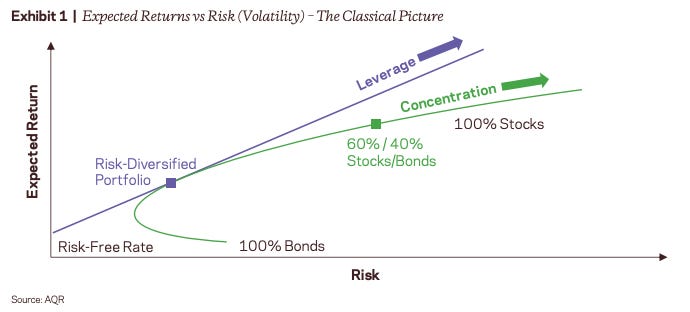

Leverage vs. Concentration

Investors prefer concentration over leverage when maximizing their expected return.

This means most of us will allocate larger and larger portions of our portfolios to stocks, expecting higher returns. In contrast, you would have gotten a better risk-adjusted return if you had a well-diversified portfolio and then leveraged that.

One key reason for increasing concentration rather than leverage was aversion to leverage. Investors believed that increasing concentration was the “natural or conventional” path to taking leverage, which felt speculative.

What’s the optimal leverage?

While there is no one right answer, leveraging 10x on the market rarely works out. That’s because if you are levered 10x and the market drops 10% (relatively common), you will be wiped out.

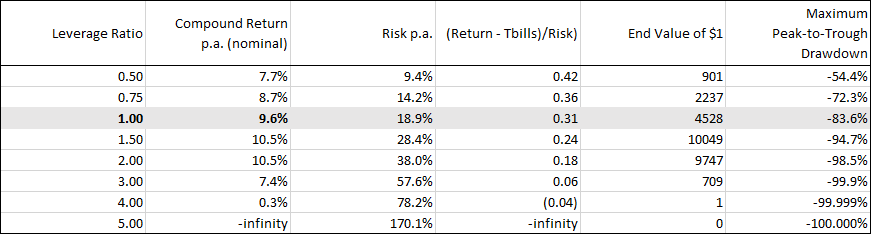

In this thought experiment by Elm Wealth, the impact of using leverage in the S&P 500 from 1927 to 2020 was evaluated.

Notice that 1.5x leverage leaves you with the most money at the end, but at some point, you’d have experienced a drawdown of 95%.

Above 1.5x leverage, return goes down and risk goes up, driven by the volatility drag we’ve been discussing.

At 4x leverage, after suffering more than a 99.99% drawdown, you’d eventually only be left with the $1 you started with (just $0.09 inflation-adjusted), and at 5x leverage you’d have been fully wiped out on October 19th, 1987.

Most studies recommend up to 2x leverage, and there are few good reasons to go above 3x.

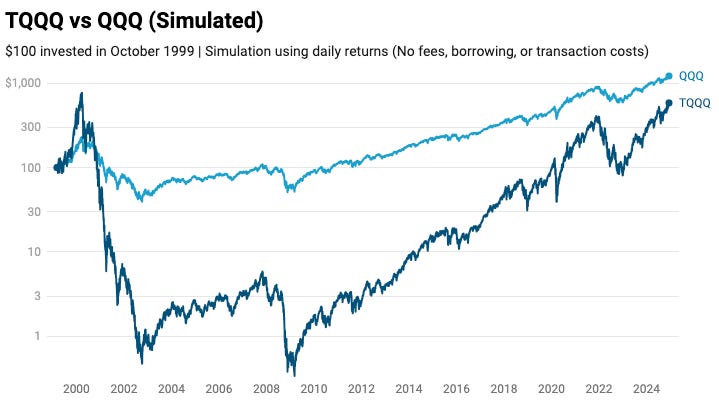

TQQQ during the Dot-com bubble and the Global Financial Crisis

The biggest concern regarding leveraged ETFs is that most of them were not present during the dot-com bubble and the Global Financial Crisis.

For example, TQQQ was launched in 2010.

So what happens if we create a simulation to evaluate how a hypothetical TQQQ portfolio would have performed?

The 3x-leveraged QQQ would have been wiped out twice — once during the dot-com bubble crash and again during the global financial crisis.

$100 invested in TQQQ at the end of 1999 would have grown ~10x by the top of the dot-com bubble in 2001. But in the crash that followed, the portfolio would have dropped to <$1. While in our simulation, the portfolio does make a comeback, we would argue that, given the transaction and borrowing costs (which we ignored here), a real fund would have been shut down.

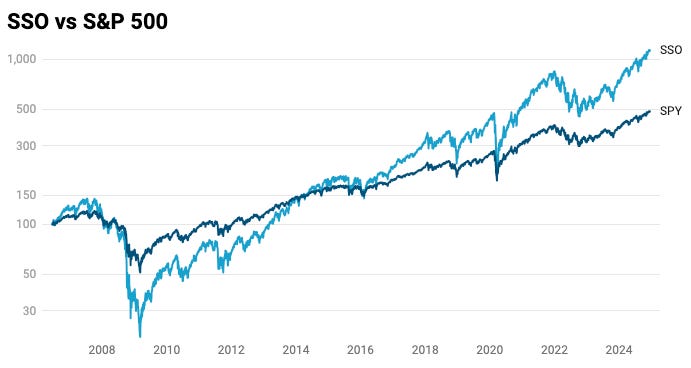

This also corroborates our earlier research, which recommends that optimal leverage be <2. Let’s take another example of a real leveraged ETF — SSO (2x leveraged S&P 500), which was launched in 2006 (before the Global Financial Crisis).

$100 invested in SSO at its launch would drop to ~$20 during the Global Financial Crisis. While this drawdown was brutal, it was not a scenario so extreme that the fund had to shut down. During the bull market that followed, the SSO portfolio overtook the S&P 500 by 2014, and by 2025, your investment in SSO would be 2x that of the S&P 500.

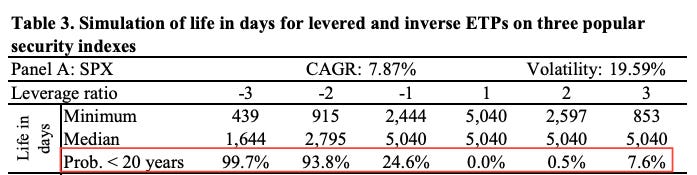

Researchers at Vanderbilt University had similar findings.

When they ran 10,000 Monte Carlo Simulations on leveraged ETFs based on the S&P 500, they found that over a 20-year period, a 2x-levered ETF had only a 0.5% probability of shutting down, and a 3x-levered ETF had a 7.6% probability of shutting down.

It’s also interesting to note that if you were 2x short the S&P 500, you had a 94% chance of the fund shutting down over a 20-year investment horizon.

Should you be investing in leveraged ETFs now?

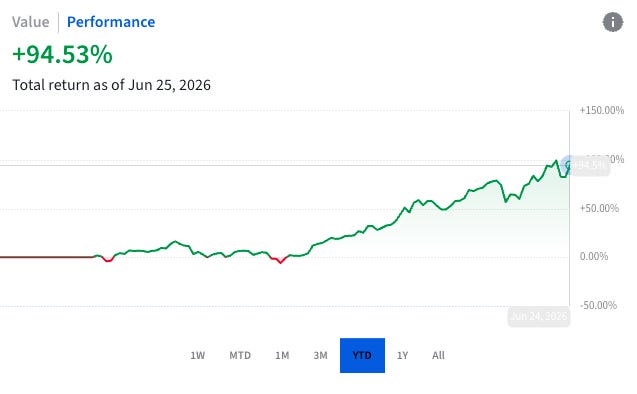

Not if you are looking at individual stocks and especially semiconductors. Not to be “that guy”, but our MS portfolio has nearly doubled YTD without touching leverage.

There is no reason to add additional risk by using 2x or 3x leverage on an already volatile name. That’s how you end up in situations like this:

Finally, you have to be aware that for leveraged ETFs to make money, it’s not enough for the market to go up; it should do so with relatively low volatility.

Volatility Drag

While most investors are worried about the fund shutting down, the real risks with leveraged ETFs lie in the volatility drag. Take our earlier example of the fund's +10% and -10% moves over 2 days. The 3x levered ETF declined 9% compared to the underlying index's 1% drop.

In extreme cases, even if the index is moving up, you will lose money due to volatility. From February 2020 to January 2023, QQQ was up 30.76%. But, TQQQ declined 11.37%. This was due to

~60% drop due to the COVID-19 crash

+200% run-up during the everything bubble in 2021

Another 50% drawdown during the 2022 rate hikes.

This incredible amount of volatility caused the 3x levered index to move very differently compared to the underlying index.

Leverage — The secret behind Buffett’s returns

Once again, it all comes down to your skill as an investor. While leveraging and investing in speculative stocks rarely works out, you can make leverage work for you if you know what you are doing.

While Buffett eschews debt publicly, a large chunk of his returns can be attributed to the smart use of leverage.

Berkshire Hathaway has realized a Sharpe ratio of 0.76, higher than any other stock or mutual fund with a history of more than 30 years.

In the famous paper Buffett’s Alpha, researchers analyzed Buffett’s portfolio to understand how he was able to generate such a high risk-adjusted return. They found that Buffett used the cheap leverage available to him from his insurance float and invested it in high-quality value stocks to generate market-beating returns.

We estimate that Buffett’s leverage is about 1.6-to-1 on average.

Buffett’s returns appear to be neither luck nor magic, but, rather, reward for the use of leverage combined with a focus on cheap, safe, quality stocks.

The real alpha might be in realizing that very few of us have the patience and the skill of Buffett.

Market Sentiment is now fully reader-supported. A lot of work goes into these articles, and if you enjoyed this piece, PLEASE HIT THE LIKE BUTTON. It’s the only way new readers can discover our reports :)

Footnotes

It won’t exactly be double as you have to pay some amount as interest for the money lent to you.

I wrote my thesis on this subject. Slow active allocation rules like selling 2x leveraged for 1x fund when hitting x volatility percentile and buying back in when we drop below the volatility percentile can GREATLY reduce downside risk.

OOS I managed to have near identical return to 2x's return, but shrunk the MaxDD from 78% to 52%