Memory Bottleneck

We're still at the beginning

We are publishing this without a paywall.

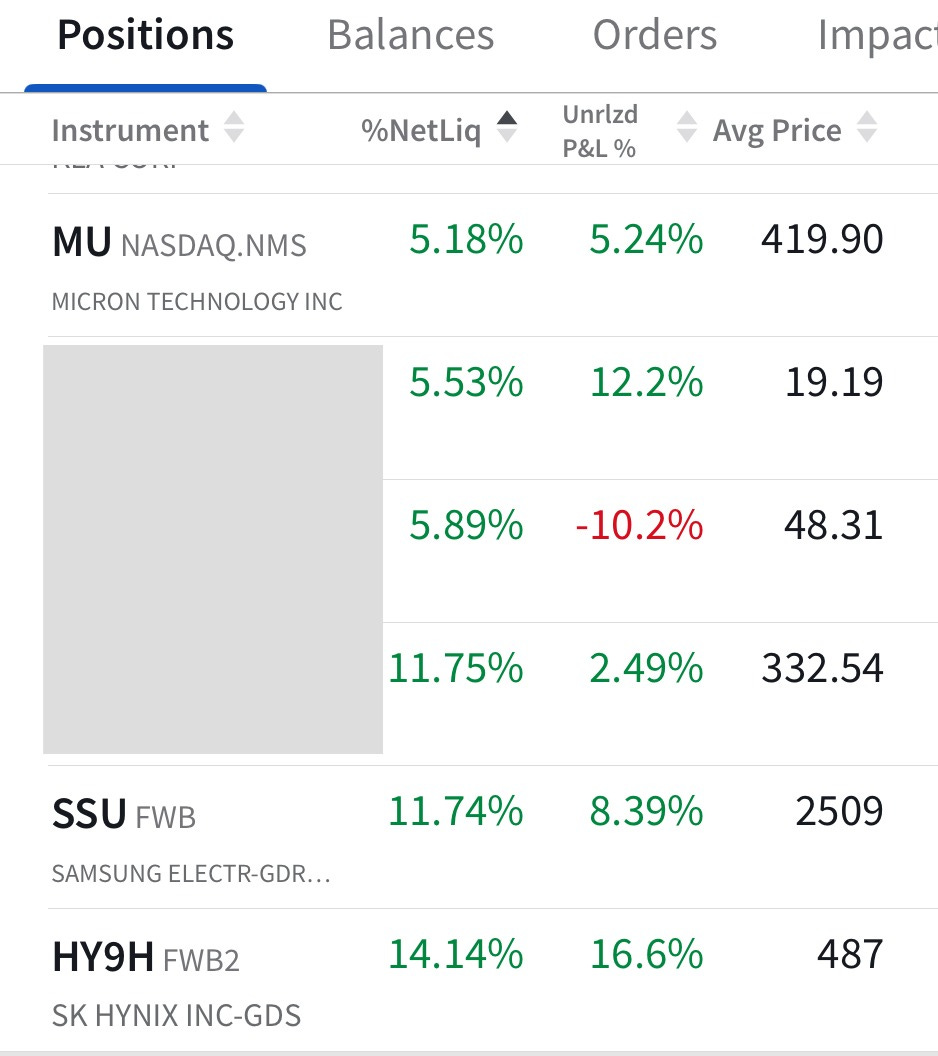

While QQQ is down 4% YTD, the Advanced Packaging portfolio we put together is now up 8%! What’s more interesting is how strongly the memory basket within the advanced packaging has performed. Our focus was solely on High Bandwidth Memory, as these three companies own the entire market:

Micron: +6%

Samsung Electronics: +30%

SK Hynix: +24%

Even with our 35% allocation to these 3 companies, we might have underestimated how much bottleneck memory (both DRAM and NAND) is now becoming to AI. With memory inventory still going down and pricing increases accelerating, let’s dig into why AI is using so much memory and how we are positioning ourselves with a memory basket.

Market Sentiment dives deep into the bottlenecks of the AI world. Join 44,000 other investors to make sure you don’t miss our next briefing.

Why memory is becoming an AI bottleneck

Have you ever had a long chat with ChatGPT or Claude where, at the end, the bot behaves like it has no clue what the conversation was about?

It’s because the model ran out of context, which it keeps in memory. Context is what the model retrieves before answering so that it can make sense of what’s going on. The longer the context window, the more useful the conversation. But on the other hand, when you double the amount of context, the underlying model needs 4x the memory.

Adding fuel to the fire are the recent breakthroughs and usage patterns in AI:

Agentic reasoning generates a long sequence of steps before giving the final answer. This means that the AI model should now retain all prior steps in memory so it has context for what it’s expected to do.

Images, audio, and video generation consume far more memory than mere text generation. For example, to ensure characters are consistent throughout an AI-generated clip, the model must retain the entire frame in memory rather than just a few words.

Finally, since model providers are pushing universal assistants that know everything about you, they now simultaneously have to keep the current conversation, general information, and old conversations to make sure the experience is seamless, which pushes the memory usage even further.

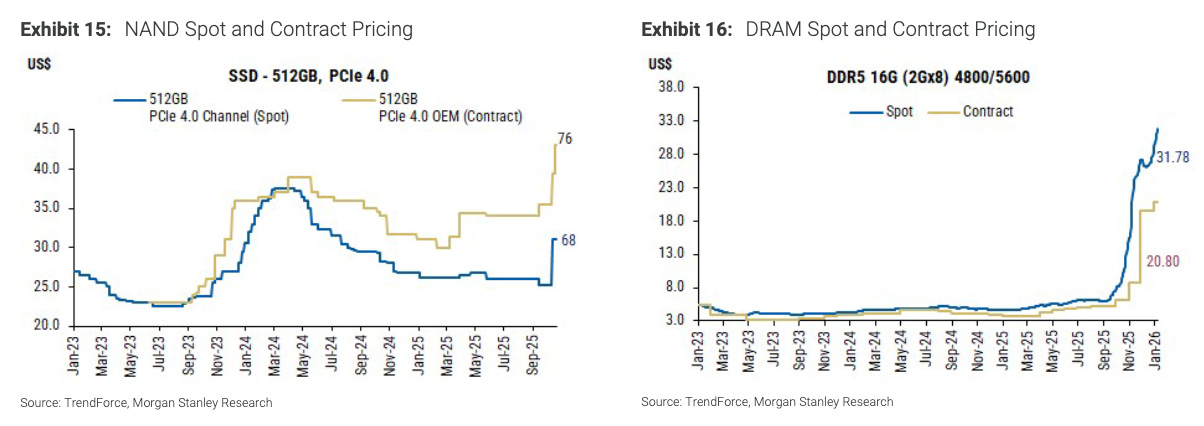

This is the first half of the problem. Keeping billions of users' full conversation histories, generated images, and agentic workflow records means that demand for long-term memory has also exploded. All this meant that the prices for both long-term (NAND) and short-term (DRAM) memory have gone parabolic.

Is this time different?

None of the above is new information to investors who are closely following the AI market. Yet, while the market (S&P 500) is trading at a forward P/E of 21x,

Micron is at 10x

SK Hynix is at 5x

Samsung is at 6x

This gap is because investors have been burned by the cyclical nature of these companies. We had a similar playbook during the Windows PC super-cycle in 1996, the cloud and smartphone boom in 2016-2019, and the COVID cycle a few years back. In all three cases, the playbook was the same.

A catalyst will cause a huge spike in demand for memory (for example, during COVID, everyone was sitting at home, and there was a rapid demand increase for gaming PCs and workstations, driving up demand for DRAM). Companies will race to build new manufacturing plants, end up overshooting demand, and crater prices.

The phrase "this time is different" is considered one of the four most dangerous in investing, for good reason. But as my friend UncoverAlpha argues in his latest report, this time it might actually be different. A snippet from his report:

In every previous memory cycle, the demand driver was the same: humans buying devices. PCs in the 1990s. Smartphones in the 2010s. Laptops during COVID. The demand function was ultimately capped by the number of humans and the number of devices each human needs. One person buys one phone. Maybe one laptop. Perhaps a tablet. The DRAM content per device grows, but the number of endpoints is bounded.

This meant that once the initial adoption or upgrade wave passed—once everyone who needed a new PC had bought one, or every smartphone had been upgraded to the latest generation—demand would flatten. Supply, which was ramped during the boom, would overshoot. Prices would crash.

In the AI era, the demand function for memory has fundamentally changed. Memory is no longer predominantly serving a fixed number of »human endpoints«. Memory, especially HBM, is now a critical input for generating intelligence.

In the PC cycle, once every household had a PC, demand plateaued. In the smartphone cycle, once penetration hit saturation, annual unit growth went to zero. But the number of AI inference calls per day is growing exponentially and is nowhere near saturation. Every enterprise, every consumer app, every autonomous vehicle, every AI agent is an incremental consumer of memory bandwidth. — UncoverAlpha

Where are we now in the cycle?

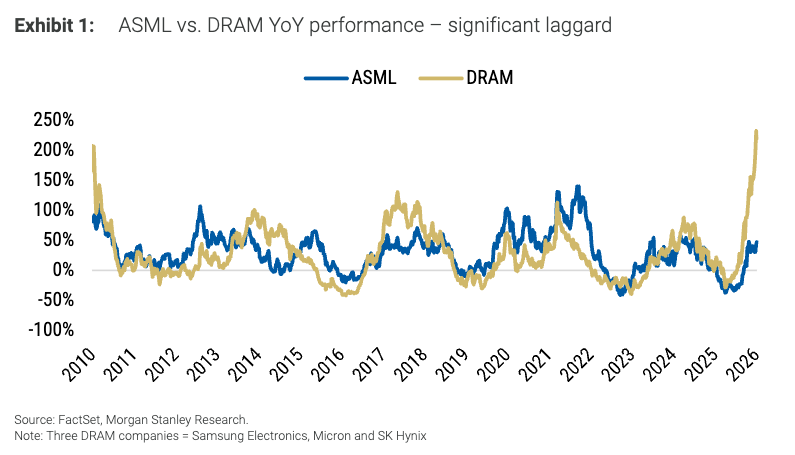

Given that all the memory stocks look like the following chart, the all-important question becomes: where are we in the cycle?

From our perspective, all the demand vectors are still largely ahead of us and not behind us. Outside of the Twitter & Substack bubble, you can rarely see someone using an “Agent” to get anything done or using an AI as anything other than a simple replacement for Google search.

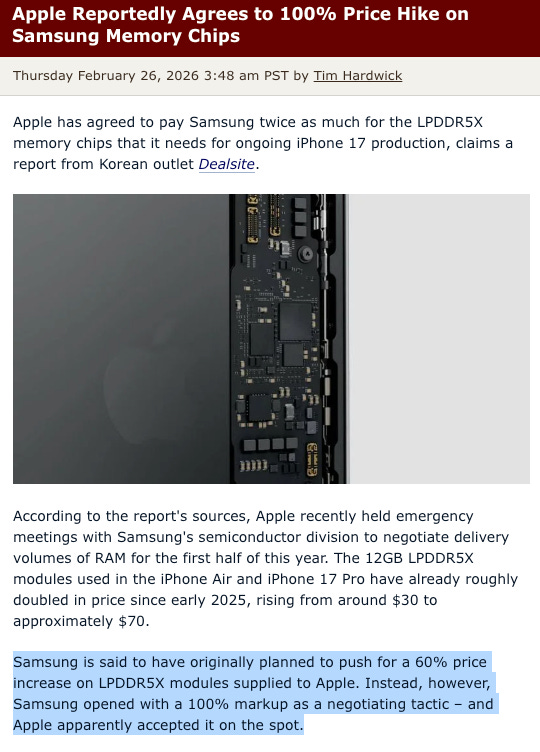

Given the capex and time required for the new facility to come online, we can safely bet that the supply side is locked in for years, while the demand curve continues to grow exponentially. Another factor that supports this trend is that the companies buying these chips have strong cash flows and good margins, which means that the memory companies can get away with incredible price hikes: Just as Samsung did last month.

How are we positioning?

As discussed at the start, we already have significant positions in SK Hynix, Samsung, and Micron as part of our Advanced Packaging portfolio (Opened on Jan 30th).

Given how severe the memory bottleneck is, it makes sense to gain exposure to a few more companies specializing in both DRAM and NAND. We are adding 10% more allocation to the memory bottleneck with the following additions:

ASML Holding ($ASML) | 5%

You can read our deep dive into ASML here (up 68% since our coverage). According to Morgan Stanley research, even though semiconductor companies experience an upturn in revenue and profitability one or two quarters ahead of the memory makers (as equipment orders are placed well in advance), there is a significant lag before their share prices catch up to those of the memory makers (we are looking to capitalize on this). If you are a value investor, you can check our valuation model for ASML 0.00%↑ here.

Western Digital Corp | 2.5% || SanDisk Corp | 2.5%

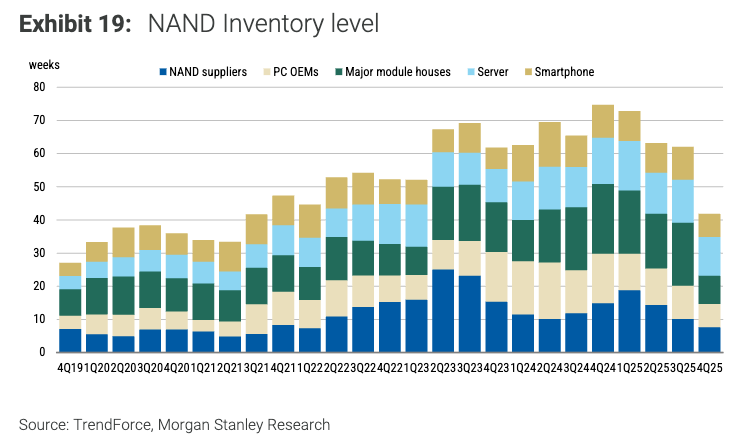

More of a momentum play than anything else. Both these companies have risen considerably over the last year (SanDisk 1088% & Western Digital 508%). These companies trade at a significant premium to their HBM counterparts (primarily because they are listed in the U.S.) and are proportionally riskier bets (hence the low allocation). The bet here is that even with the price hikes, NAND inventory levels have kept falling, so we might not be at the top of the cycle.

Before you go

Unlike our Energy and Optics portfolio, this is not a long-term trade you can buy and forget, and comes with a visible expiration date. The bull case for memory will only hold as long as these 3 conditions remain intact:

Declining inventory: Hyper-scalers are still stockpiling, and we see no line of sight on inventory bottoming. Until we do, demand is structurally outpacing supply.

Accelerating YoY pricing: Pricing for DRAM and NAND is expected to rise into Q2 2026, with potential for a 20% hike in Q3, which shows us that the pricing cycle has not peaked.

Stocks still rewarding good news: All strong results are met with the stocks pumping and not sell-the-news behavior.

Any one of the above conditions breaking would be a good signal to exit the trade. As always, we will continue to monitor these conditions and update our subscribers. Consider upgrading your subscription to get these updates!

More interesting reads

That’s it for now. If you are here, please “♡ Like” this piece. It helps us massively!

Disclaimer: This is for informational and educational purposes only and is intended solely for readers in the United States. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance may not repeat itself.