Notes on Memory

Still think its cyclical?

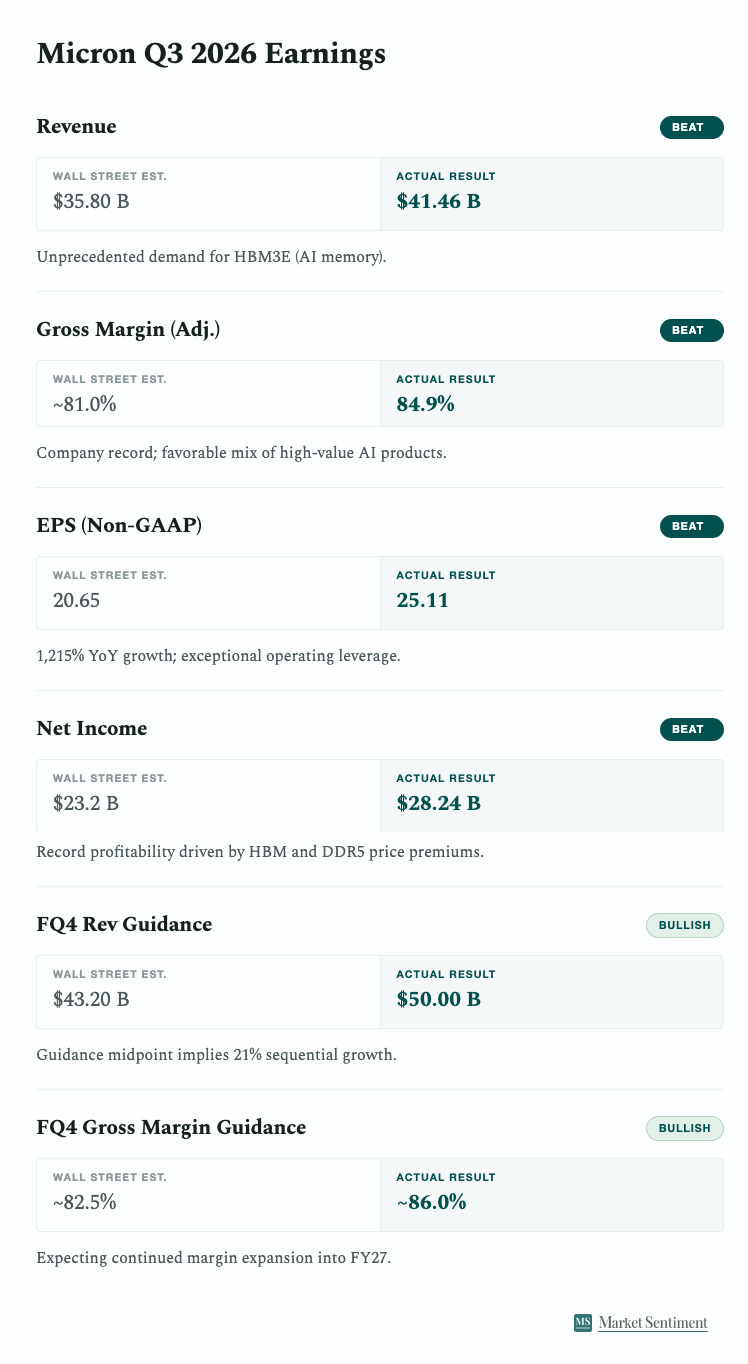

Micron Technology announced blowout earnings, and the stock is up 18% in after-hours trading. The numbers are staggering:

Quarterly revenue: $41.5B (up 340% yoy)

Guidance for next Quarter: $50B (Estimate was $43B)

16 long-term contracts worth $100B+

Since the beginning of the year, we have consistently highlighted that memory has shifted from a cyclical product to a structural need for hyper-scalers, and Micron’s latest earnings prove it.

Why AI needs memory?

Reiterating our demand drivers from our memory bottleneck post,

Agentic reasoning generates a long sequence of steps before giving the final answer. This means that the AI model should now retain all prior steps in memory so it has context for what it’s expected to do.

Images, audio, and video generation consume far more memory than mere text generation. For example, to ensure characters are consistent throughout an AI-generated clip, the model must retain the entire frame in memory rather than just a few words.

Finally, since model providers are pushing universal assistants that know everything about you, they now simultaneously have to keep the current conversation, general information, and old conversations to make sure the experience is seamless, which pushes the memory usage even further.

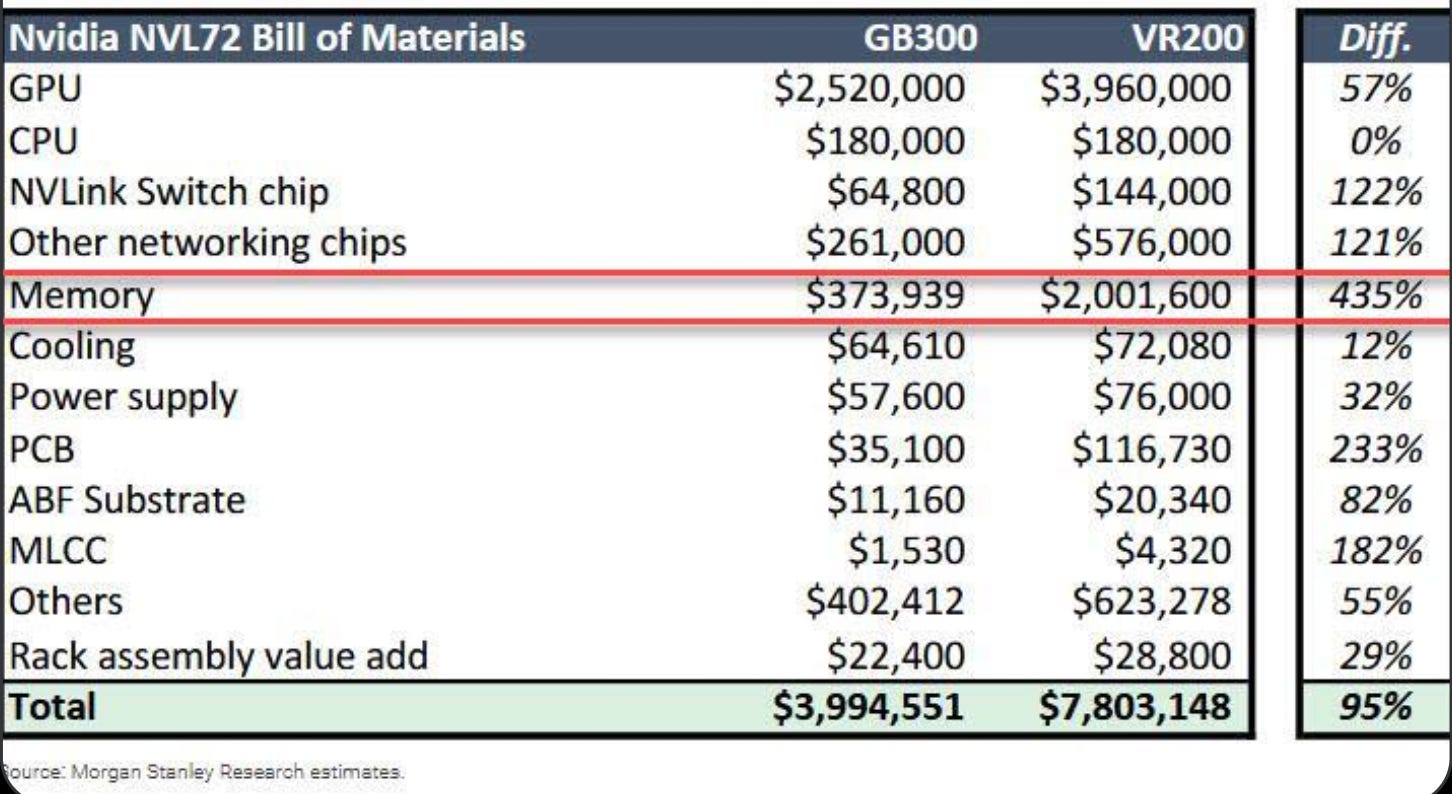

Nvidia’s own bill of materials tells the same story. The 2025 GB300 NVL72 rack carries about $374K of memory — roughly 9% of its ~$4M total cost. Just a year later, next-gen VR200 packs roughly 3x the memory capacity at roughly 2x the price per GB, pushing memory cost to ~$2M — a 435% jump that brings memory to ~26% of AI server cost.

New demand vectors

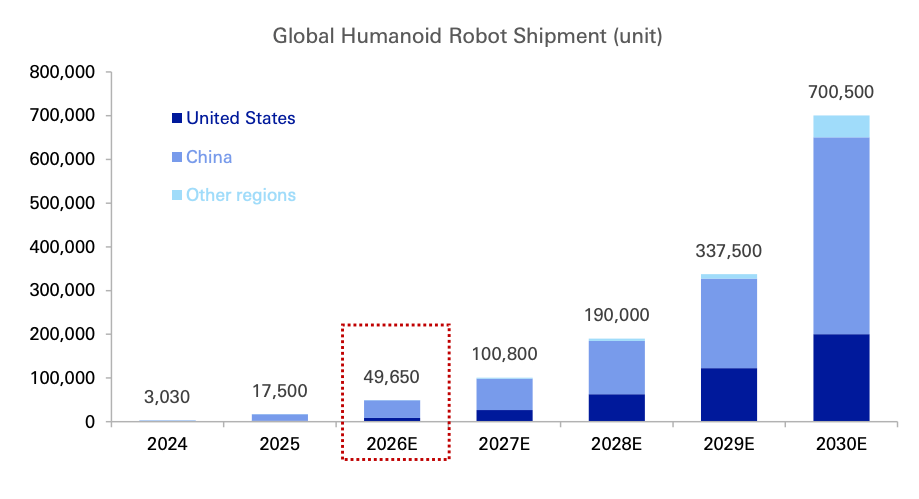

In the earnings call, Micron CEO Sanjay indicated memory demand for a robot is 10x that of an autonomous car. And these robots are expected to grow exponentially as the price per unit falls and they can tackle general-purpose tasks.

Powered by these tailwinds, we believe Memory will stay in a supercycle for years. That conviction is shared. Sixteen companies, including two hyperscalers, signed long-term agreements with Micron to lock in supply for three to five years. Traditional memory deals run two to three quarters at most — the shift reflects a long-term supply crunch.

These contracts cover advanced memory products and account for roughly 25% of Micron’s supply volume and 40% of its revenue at current prices. This is bullish for Micron as it secures prices and profit margins for the next three to five years.

The biggest issue with memory stocks was their cyclicality. Just 4 years ago, Micron’s gross margin went from the high 40s to near -31%, with Micron selling memory below cost due to oversupply. These long-term contracts prevent a similar downturn — The largest agreements carry a ceiling at the current CQ2 market price and a floor that holds through the term.

Even at the floor, Micron expects a gross margin well above its prior peak quarterly margin of roughly 61%, which puts the floor north of 65% on our estimate.