One Year of Rebound Capital

Take a simple idea and take it seriously

Hi there,

This is a guest post from Rebound Capital. We launched Rebound Capital last June as our equity research division after more than 4 years of research at Market Sentiment. Here’s the one year update (and a special offer for Market Sentiment readers who make it till the end)

On June 5, 2025, we launched Rebound Capital. It was the culmination of more than 4 years of research at Market Sentiment, where we evaluated everything from investing in companies more than 100 years old, to economic moats, to tracking insider trades by members of Congress.

There’s this one idea we always came back to: investing in quality companies in a drawdown.

Here’s what we wrote about Meta in 2022:

No matter how you look at the company, the financial metrics are incredible. 80% gross margin and 30% ROE with growing revenue. But the stock is down 55% in the last 1 year.

I am not pitching it as a great business. They certainly have some incredible challenges ahead of them in terms of privacy and attracting a young user base. No one knows directly the solutions for their hardest problems—that’s why they’re the hardest ones.

But writing off a company based on two bad quarterly reports is just too short-sighted.

The same theme kept recurring:

Netflix lost 3/4th of its value because it did not grow subscribers one quarter.

ASML lost ~1/2 its market cap on tariffs and export restrictions.

Amazon was down 56% after its first quarterly loss since 2015.

So we finally pulled the trigger and launched Rebound Capital, putting our own capital on the line. We followed Charlie Munger’s advice of “take a simple idea and take it seriously” and spent the past year going through hundreds of stocks to find the optimal rebound setups.

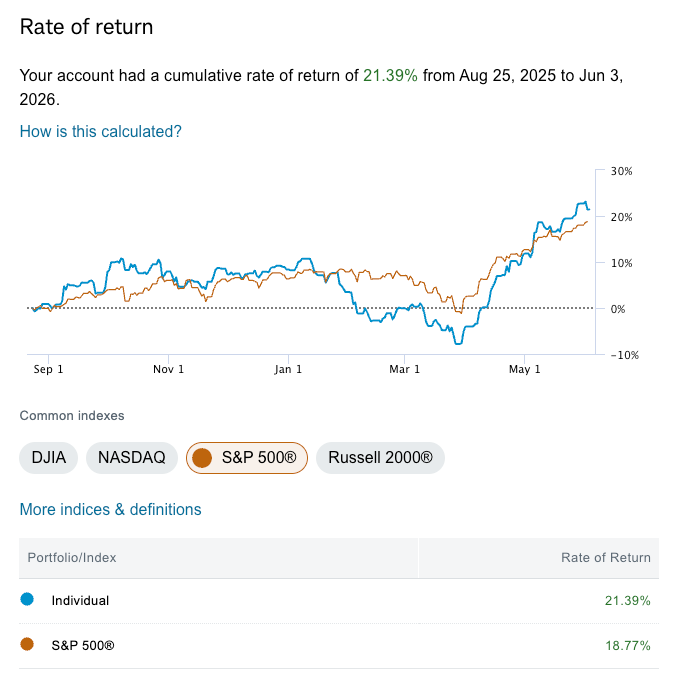

Fast forward a year, and we are outperforming the S&P 500 while holding top 3 positions in relative value names such as Amazon, Constellation Software, and MercadoLibre. To put this in context, 79% of all active large-cap U.S. equity funds underperformed the S&P 500 last year.

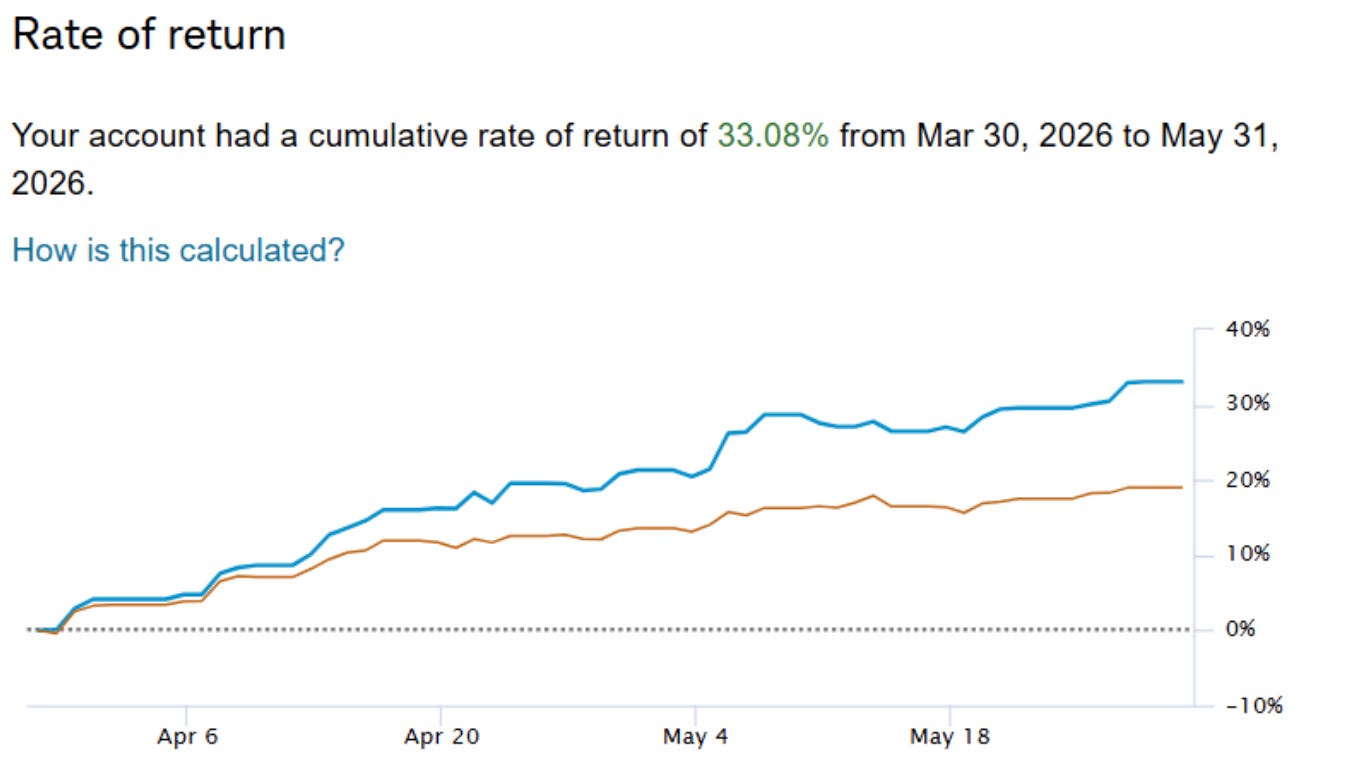

While it’s easy to talk a good game when your portfolio is outperforming, sticking to the strategy when it’s underperforming is the hardest thing to do as a public facing equity research platform. Q1 was hard on the Rebound Portfolio, where we underperformed the market by 9%. We continued to share our portfolio performance publicly throughout the period of underperformance (here are our Feb, Mar, & April updates). But sticking to our strategy helped us double down on quality names that rebounded strongly after the March dip.

Not to name names, but there are a lot of “gurus” who have Excel spreadsheets where the portfolio never goes down, and they magically exit at the right time. For us, we have maintained the policy of informing you of all our trades 24 hours in advance, and honestly, our biggest success till now is that nobody has ever said anything bad about us.

Overall, we are now in a good position with our portfolio compounding faster than the index while trading at essentially the same valuation. The headline numbers (weighted average of our portfolio holdings):

Revenue growth, next 3 years: ~18%

EBIT growth, next 3 years: ~19%

EV/EBIT: ~27x, in line with the S&P 500

Here is the unusual part. We own a basket whose EBIT is set to grow ~19% per year over the next three years, compared with <13% for the S&P 500, and we pay no premium on the multiple to do so.

Divide valuation by growth, and the portfolio sits at ~27/19 = ~1.4, versus 27/11 = ~2.5 for the index (lower is better). In short, our portfolio compounds faster than the market while costing about the same, which on a growth-adjusted basis makes it materially cheaper than the index it is built to beat.

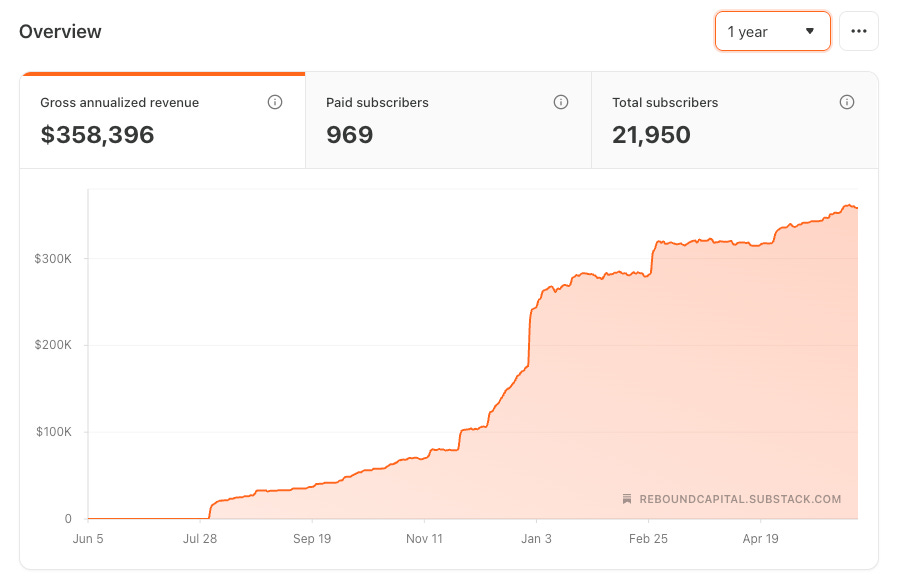

Your support has been incredible, and it’s what makes this work feel meaningful. While most creators are hush-hush about how much they make, we are going to show you our real numbers. After all, this is the easy bit after sharing our portfolio performance :)

As of today, we have more than 21,000 investors who subscribe to us, of which 969 investors pay to read our research, which translates to revenue of $358K (ARR). The spike you see in December is when Michael Burry became a paid subscriber to Rebound Capital and endorsed our note on Birkenstock.

Consider this your nudge to put your own work out in public. You never know who’s reading.

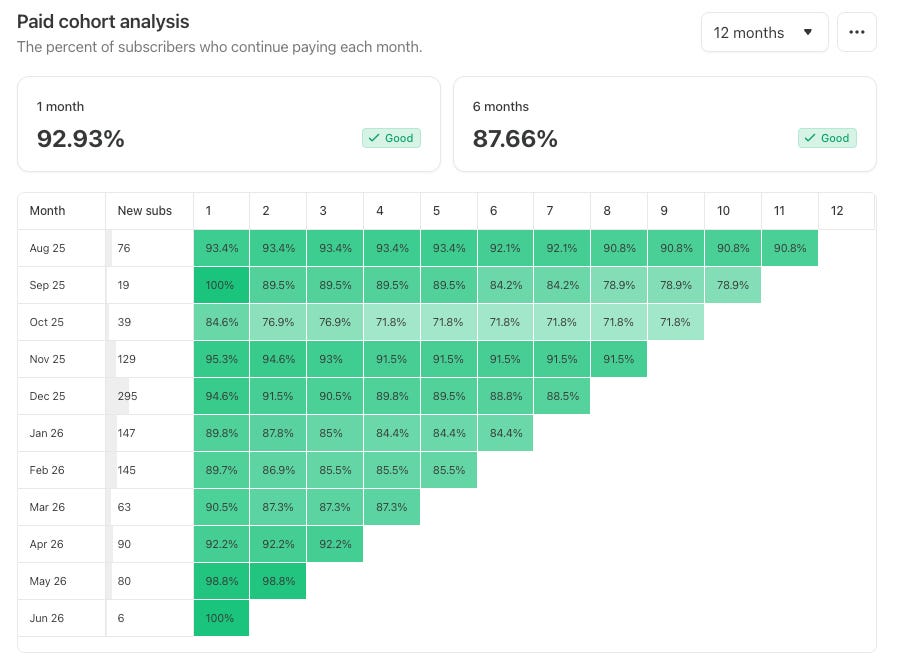

Finally, of all the metrics at Rebound Capital, our retention rate is the one that we are most proud of. ~90% retention at 6 months is unheard of in the newsletter space and is the best testament to the quality of the research we produce and the value you derive from it.

Right now, the market is in love with AI. Money is pouring into a narrow group of names at prices that already reflect the next 5 years of growth. To be clear, we are bullish on what AI can do over the long run. But when an equipment vendor that has always been cyclical gets priced as if the cycle has ended, the reward for chasing it is small, and the cost of being wrong is high. With many indexes changing their decade-old rules to accommodate hyped-up IPOs like SpaceX, indexing is no longer the safe, neutral choice. The case for doing your own research only gets stronger from here.

And this is where being independent matters. A fund manager has to answer to a committee, hug the benchmark, and own the hot name so they don’t look wrong at the next quarterly review. We answer to no one but you. We never have to chase the story of the moment and can sit in an out-of-favor name and wait for the market to catch up, because no one is going to pull our capital for being early.

While investors flock to one part of the market, high-quality companies are being ignored. Some of the best compounders we know are at their lowest multiples in years. We will continue to focus here. The crowd overpays for what it loves and ignores the good businesses on sale. But the market eventually catches on.

So we will keep researching the names nobody wants to talk about. The rotation back to high-quality names will come. Our job is to be patient enough to hold the right names when it arrives.

Anniversary Offer from Rebound Capital

To celebrate one year of Rebound Capital, we are offering 33% off to all current subscribers of Market Sentiment. This offer is valid only for the next 24 hours and if you are an existing reader of Market Sentiment.