Tail Ends

Hedging for the outliers

Welcome to the 400+ investing enthusiasts who have joined us since last Sunday. Join 28,050+ smart investors and traders by subscribing here. It’s totally free :)

I had a funny feeling in my gut, I didn’t want to make a mistake. I made a decision, and that was it - Stanislav Petrov

It was Sep 26th, 1983, and the Cold war was at its peak. Just 3 weeks earlier, the Soviets had shot down a commercial flight killing all 269 people on board, including a Congressman from Georgia. President Ronald Reagan had declared the Soviet Union an “evil empire” and had announced the Strategic Defense Initiative which aimed at shooting down missiles before they reached the U.S (mockingly dubbed “Star Wars”).

Stanislav Petrov, a 44-year-old lieutenant colonel in the Soviet Air Defense Forces, was in the middle of his shift as a duty officer for the Soviet early warning system for Nuclear launch. The system could predict with “high reliability” if an American intercontinental ballistic missile (ICBM) had been launched and was headed toward the Soviet Union. Suddenly, the alarms went off and the system reported that a total of five Minuteman ICBMs had been launched by the U.S against the Soviets.

Petrov had an important decision to make - Report the attack to his superiors virtually guaranteeing a full-scale Nuclear counterattack or, go with his gut decision that it was probably a false alarm by the newly deployed system. He went with the latter and even as the computer alerts in front of him changed from “launch” to “missile strike,” and insisted that the reliability of the information was at the “highest” level, he stuck to his gut and did not report it.

In the end, Petrov turned out to be right1 - It was a false alarm and was triggered when Soviet satellites mistook the sun’s reflection off the tops of clouds for a missile launch. It’s estimated that he prevented more than 2 Billion deaths with his action. The probability of a full-scale nuclear war is extremely low but, the consequences, if it happens, are unimaginable.

Similarly, in investing, its always a few events that would make or break your entire portfolio. The Dow industrials dropped ~13% in one day last March and S&P 500 went on to drop 34% in 4 weeks due to the Covid crisis. The last 10 years leading up to the 2007 Housing market crash made us believe that there is no way that home prices are going to drop. Then it dropped by 30% in one year.

Given that the tail-end events are what matter2 , what if there was a way to hedge against these risks? Just like how we buy insurance for our houses & cars, what if we could buy insurance for our portfolio?

Tail Risk Hedging

The strategy in theory is very simple. You buy Put Options (the right to sell the index at a specified price) well below the current market price. In normal environments, the volatility of the market is very low, and buying short-dated puts that are way out of the money is very cheap.

For example, if you are buying a $SPX put today with 31 days to expiration, the following are the bid and ask for varying strike prices3.

As you can see, if you want to hedge for a 4% drop, you need to pay ~7x more than if you are hedging for a 16% drop. The massive difference in premium is because, based on historical data, a 16% drop would be much rarer than a 4% drop within a month.

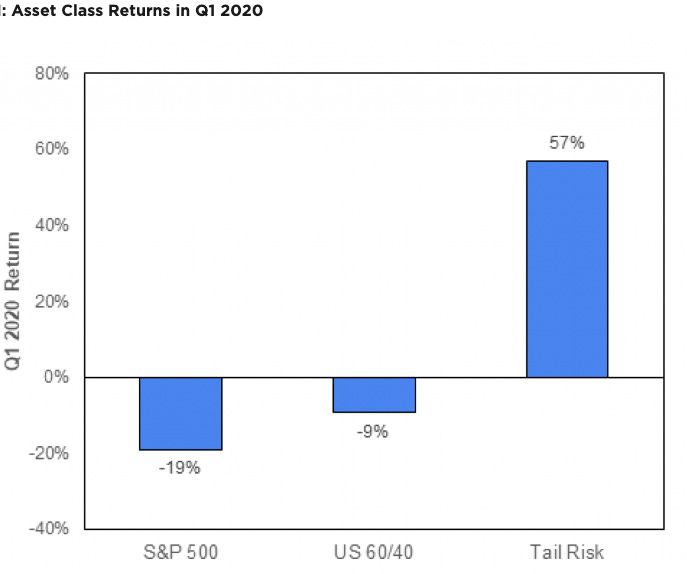

This is the exact strategy that Mark Spitznagel’s $4.3 billion Universa Investments used to make a 3,612% return in just one month during the Covid crisis. They make trades that almost always lose money - since you are betting on an extremely unlikely event to happen, most of the time, it won't occur - making your Puts worthless. But, once in a while, something so crazy happens (Pandemic, 9/11, 2008 crisis, etc.) that your Puts become incredibly valuable offsetting all your previous losses. (In the case of Universa, they started in 2008 and had to wait 13 years for the next crisis to unfold)

Warren Buffett would attest that running an Insurance company is an excellent business long-term. If the companies are charging the right premium, they can create massive profits as the premiums would far exceed the payouts over the long run. So, if you are someone who is taking insurance, your expected long-term value is negative4.

The same problem is applicable to Tail Risk Hedging.

We know that the stock market has trended upward over the past century and has a positive expected return. So buying Puts is a losing strategy long-term and that’s exactly what we see from the data. Buyers of tail risk funds have historically paid about 3.4% per year to make 25–50% in crises. These strategies in general carry a negative long-term expected return.

If you are like me and are thinking of “gaming the system” and getting into tail-risk strategies only during periods of crisis, it would not work. The premiums for buying the put options would spike up during periods of turbulence - It would be akin to trying to buy health insurance while you are in the hospital.

We spent the last decade debating whether economic risk meant the Federal Reserve set interest rates at 0.25% or 0.5%. Then 36 million people lost their jobs in two months because of a virus. It’s absurd. - Morgan Housel

The Tail Risk hedging strategy is definitely not for the faint-hearted. You would have to take years of continuous loss before an inevitable crash pushes your portfolio back to green.

The closest ETF that I could find that follows this strategy is Cambria Tail Risk ETF. They invest one percent of their holdings every month in out-of-the-money put options on the S&P 500 Index. The fund did rise ~25% during the Covid crisis but over the last 5 years, it has an annualized return of -6% compared to +9% of the S&P500.

My take on investing in this strategy is very close to what I recommended for the Permanent Portfolio. If your investment horizon is extremely high (20+ years), just sticking to equities is the best bet for long-term wealth creation. If you need your funds in the next 5 years or are planning your retirement soon, a tail risk strategy can help prevent nasty surprises.

This publication remains free due to support from our partners. Do check out Percent.

Footnotes

Even though he was right, he was relentlessly interrogated and was never rewarded for his decision by the Soviets. It took more than 20 years for the world to know his story.

Just in the last 2 decades, we have been through 9/11, the Housing market crisis, and a once-in-a-century Pandemic.

Source - You can read up on Put Options if you are not clear on how they work.

Which is to be expected - We take insurance for peace of mind. Nobody would take car insurance hoping for a car crash!

If you enjoyed this piece, please do me the huge favor of simply liking and sharing it with one other person who you think would enjoy this article! Thank you.

Disclaimer: I am not a financial advisor. Please do your own research before investing.

Loved it. In regards to tail hedging funds, have you investigated the Simplify funds run by Mike Green? One of his ETFs has a semi-hedged strategy. I can't remember the full details but I think it's always buying slightly OTM puts so that it will only decline by so much in a given period.

Hey, I believe Nassim Taleb invested using these types of strategies.

I would be interested in seeing an analysis of how such a fund could be profitable.