The individual investor

What it takes to outperform

The most common argument for investing in Index Funds goes something like this: Actively managed mutual funds employ the brightest minds in the country, have access to the latest information and technology, and can employ huge capital that moves markets – if active funds still underperform the market despite these advantages, what hopes do individual stockpickers have?

The flaw in this argument is that it overlooks the advantages retail investors have over managed funds precisely because of their size. Retail investors aren’t under pressure to meet quarterly targets. Their portfolio can have a high “active share,” concentrated in a few investments that deviate widely from the benchmark. Retail investors rarely move the market with their trades, enabling covert strategies.

Yet, the question remains:

Can individual investors beat the market?

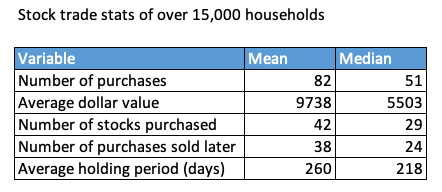

The short answer is: Yes. In a study of over 15,000 households over 6 years at a major discount brokerage, 10% to 20% of individual investors had a persistent track record of beating the market. The top decile of investors earned average abnormal returns of 6% per annum. At the same time, the bottom decile of investors consistently underperform the market. A portfolio strategy that imitated the successful investors and shorted the unsuccessful investors delivered 7% per annum abnormal returns over the market.

The study tested investor performance for both short-term trades and long-term investments. For short-term investments, investors were classified into different groups based on how their stock picks performed in a given week – then the performance of those stocks was also tracked in the next week. There was a 5-10% correlation in performance for individual stock picks implying that the short-term performance had a skill component. This skill was found to be primarily due to stock selection rather than market timing.

The difference in short-term returns due to skill is huge – between the top decile and the bottom decile, there was a spread of up to 130% over one year! There’s a possibility that the difference in performance is due to insider information rather than investor skill, so to test for this, the researchers repeated the study by eliminating multiple trades in the same stock from the sample set – this reduced the spread to ~50% per year, but the difference in skill persists.1

Long horizon performance: The same study was repeated over the entire 6-year period, looking at the complete holding period of the stocks in the investors’ portfolios.2 The top decile has an outperformance of 6% in this case and the spread between the top and bottom deciles is 9-10%.

The average investor

The above study gives evidence that some individual investors are more skilled than others, and 10-20% of investors tend to beat the market. But on average, investors tend to underperform the market. Though the top decile outperforms the market, about 50-60% of the sample underperformed the market after adjusting for risk. The bottom 30% of the sample underperformed by as much as 20-40%.

Barber and Odean studied the behavior of the average investor and observed the following:

Stocks bought by investors underperform stocks sold by an average of 2.76% per year after the transaction.

Stocks that are heavily bought by the average investor tend to outperform the market in the next few weeks – but individuals rarely capture this outperformance because their average holding period is 16 months.

Trading tends to hurt performance in general, with trading costs and commissions off-setting profits.

Here’s what the successful individual investors do differently: