MS 101

A subscriber's guide to Market Sentiment

Hi there,

Quite a few of you have joined us over the past week (we were #5 in the Rising Finance Bestsellers) and here’s a guide on what we do at Market Sentiment and how to use the subscription effectively.

Investing in asymmetric opportunities

There are only two ways to make consistent alpha in the market:

Be early

Be contrarian

It’s futile to look at a company that’s covered by 20 analysts and expect to find something that all of them have missed. Our focus at Market Sentiment is to be early to trends that are going to define the next few years.

Whether you like it or not, that trend right now is AI. We are pumping a mind-bending amount of capital into compute. To put things in perspective (all figures adjusted for inflation):

Every month, we are spending more on AI infrastructure than the total cost of the Manhattan Project.

Every quarter, we now allocate more to AI than the entire 14-year Apollo program.

Just last year, we spent more than what it took to build our entire Interstate highway system over three decades.

AI is the consensus trade now. But you can still be early to what it depends on. Capital at this scale never flows evenly. The railroad mania of the 1800s bankrupted most railroads but made fortunes for the companies selling steel and rights of way. Every infrastructure boom in history worked this way.

The AI buildout will be no different. The hyperscalers spending hundreds of billions will not be where the returns concentrate — that trade is long over. The returns will concentrate at the bottlenecks that these companies can’t sidestep. Our focus is to find them before the market prices them in.

Thematic Coverage

We have built five thematic baskets to date. Three of the five have already re-rated. Energy and Agentic AI have not, which is why they are worth a closer look right now.

Energy — AI needs energy. A lot of it. And more importantly, it needs it now. The power demand for data centers is expected to grow 10x the historical generation capacity growth. This is the one basket that’s underperformed (4% vs 15% for the S&P 500), and the reason was a simple mistake: we underestimated how fast the price of power would turn political, and over-allocated to companies exposed to electricity prices. The fix is just as simple: strip those out, and the rest of the basket handily beats the market (more on this below).

Optics — We were one of the first to cover the Optics trade last year. While the tech behind is complex, our thesis was simple: As models become more powerful and AI pushes data transfer speeds higher, the industry has no choice but to adopt optical interconnects. The basket has now rerated and is up 75% vs. 16% for QQQ.

Advanced Packaging — Once transistor shrinks stopped being cheap, the industry stopped chasing smaller nodes and started gluing chips together. Advanced packaging became the way to keep Moore's law alive, and the bottleneck moved from the wafer to the package. The basket is now up 102% vs 15% for QQQ.

Memory — Everyone knows memory stocks are cyclical and have burned investors before. But that’s the wrong question. The right question is whether we’re in a structural shift — and the data says yes. We made memory our highest allocation (34%) and were handily rewarded with a 134% weighted return (we bought the dip during the Iran war).

Agentic AI — We are at the inflection point for Agentic AI. Most AI conversations right now are about coding assistants, but that’s really only useful for the ~25 million developers out there. With Claude now generally available in Microsoft Office, AI can meaningfully support the 1.4 billion knowledge workers who spend their days buried in email, spreadsheets, and jumping between a dozen tools.

MS Portfolio

Our portfolio is where we put capital behind these emerging trends. Below you'll find every position, its current buy/sell/hold rating, and all the changes we've made along the way. If you're just starting out, begin by gradually allocating to our buy-rated names — these are the companies we still consider undervalued.

Two important notes:

Many of you have DM’d us asking how you should allocate. As much as we’d like to help, we’re not financial advisors and can’t give customized allocation advice. What we can share is exactly what’s in the sheet: our positions, allocations, and buy/sell/hold ratings, plus how we think about each of them in our deep dives.

Starting Monday, this sheet moves behind the paywall. Our full portfolio, including positions, allocations, and ratings, will be available exclusively to paid subscribers. If you’ve been on the fence, this week is a good time to upgrade.

What’s coming?

Which brings us to the good stuff. There are two big themes that we have been tracking for a while and will be sharing with you over the next few weeks.

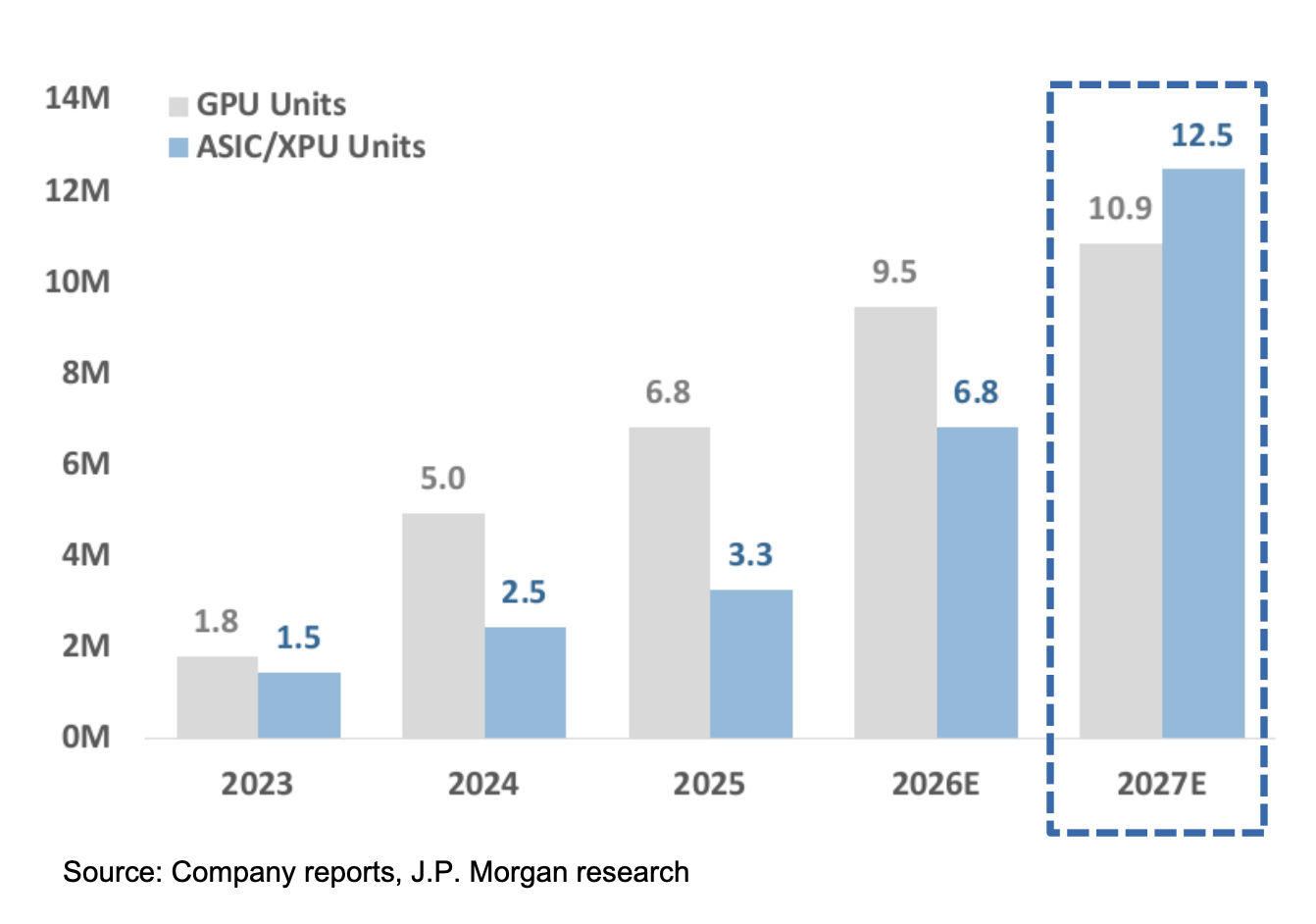

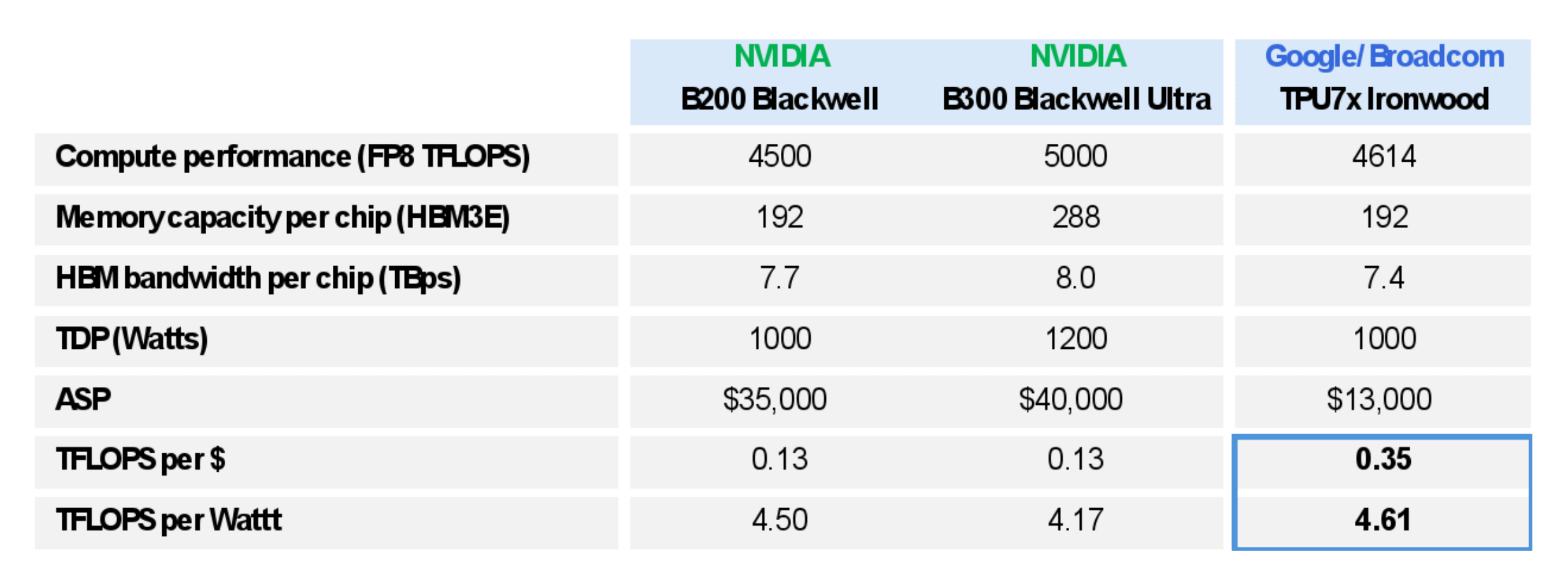

1. ASICs

ASICs (Application Specific Integrated Circuits) are projected to overtake GPU unit shipments by next year.

ASICs are chips custom designed for one specific workload. Because these chips are tailored at the transistor level, they are highly efficient at the task its designed to do.

Google’s TPU7x matches NVIDIA’s B200 on raw compute at roughly a third of the price: ~$13,000 per TPU vs $35,000.

The catch here is that ASIC development is a multi-year, multi-billion-dollar project that only hyperscalers like Google and Amazon can afford. But that’s exactly who is building them. As model winners emerge and applications standardize, ASICs lead the next wave of compute growth.

Here’s how we look at the ASIC supply chain: design tools (Cadence, Synopsys), design services (AVGO, Marvell), and licensed IP blocks (Arm, Aspeed).

The real prize sits with the designers. Complex AI ASIC design is effectively an AVGO–Marvell duopoly. This lets them charge fixed development fees plus a variable price per chip.

Given ~95% unit growth and per-chip pricing power, AVGO and Marvell earnings should see superior earnings growth over the next 2–3 years. AVGO expects its AI semiconductor revenue to grow from approximately $20 billion in FY25 to over $100 billion in FY27 primarily driven by these ASICs.

When your data-center investments run into hundreds of billions, spending a few billion on a custom ASIC is a no-brainer.

2. Energy

One mistake we made with the energy basket: we expected power prices to keep rising as demand scaled. Demand did scale. But power prices became a political problem rather than a supply-demand equation. In January, the governors of all 13 states in the PJM grid region, along with the Trump administration, jointly declared that power prices needed to be reined in and that data centers should pay for the grid costs they create. The price ceiling on capacity auctions was then extended to 2030, taking the best-case scenario we had modeled for these companies off the table.

The fix is to separate the demand thesis from the price thesis. The demand thesis was right and remains right. The price thesis is now capped by regulators until 2030.

So we are restructuring the basket around companies that get paid on volume, not price. That means the companies selling the physical building blocks of the grid: gas turbines, transformers, switchgear, high-voltage cables, backup power, and cooling systems, along with the contractors who install all of it. A transformer sold to an Amazon data center faces no price ceiling, because voters don’t pay for it.

That’s it for now. Leave a comment if you have an idea/theme that you think we all should be looking at.

Disclaimer: Market Sentiment work is provided for informational purposes only, is intended solely for readers in the United States, and should not be construed as legal, business, investment, or tax advice. You should always do your own research.