MS Portfolio Update | July 2026

The CapEx is worth it?

It’s always either peak optimism or peak pessimism in the AI world. Last month was relatively tame for AI, as all the attention was captured by the SpaceX IPO. Memory trade is still going strong, with Micron coming out with a monster quarter and SK Hynix filing the largest ADR listing in history.

What’s more interesting is the shift in mainstream sentiment. It has moved from “AI investment is setting cash on fire” to “maybe these trillion-dollar companies aren’t spending for nothing.”

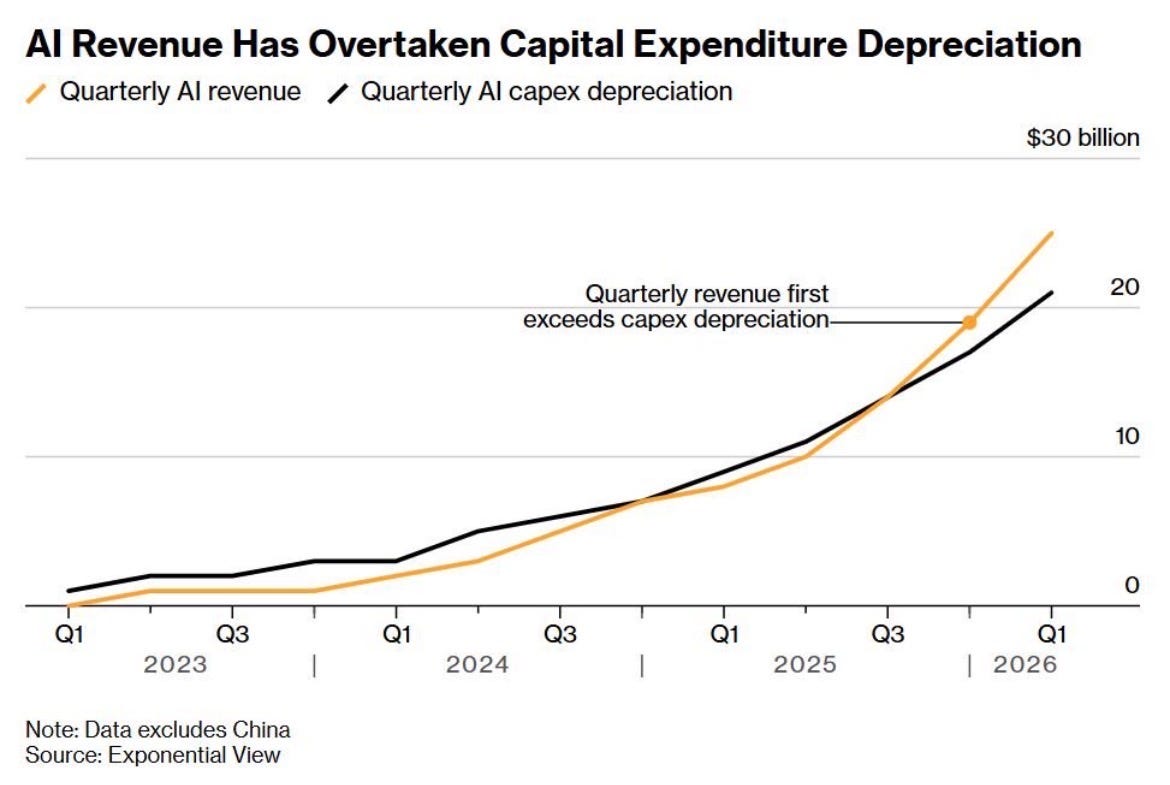

Take the chart below from the FT:

While estimates should always be taken with a bucket load of salt, it’s worth digging into what they are projecting:

The CapEx is expected to plateau (not drop) — Once you get past 2027, the CapEx is expected to stop growing at 70 to 80% a year that we are seeing now and settle into a maintenance plus refresh level.

Revenue will catch up quickly — If inference, cloud, and ad monetization compound while CapEx flattens, operating cash flow keeps climbing.

Finally, CapEx is paid upfront but counts against profits gradually in the form of depreciation over the life cycle of the asset. As the accumulated asset base grows, the depreciation add-back in the FCF bridge gets very large.

If this plays out and free cash flow explodes, the multiples will re-rate immediately. These names now carry a discount due to CapEx uncertainty. When quarterly prints start confirming that capex is flattening and cash is converting, the uncertainty discount will lift and the multiple will expand.

While all 3 are projections, we have some signs of revenue catching up. Bloomberg reported last week that AI revenue has now caught up with the quarterly CapEx depreciation. If the revenue trend holds while capex plateaus, it confirms that the trillions hyperscalers poured into AI capex were worth it.

Global AI sales, excluding China, reached $25 billion in the first quarter of 2026, exceeding the industry’s estimated $21 billion in depreciation costs tied to investments in data centers and chips for the second consecutive quarter. — Bloomberg

Market Sentiment dives deep into the bottlenecks of the AI world. Join 46,000 other investors to make sure you don’t miss our next briefing.

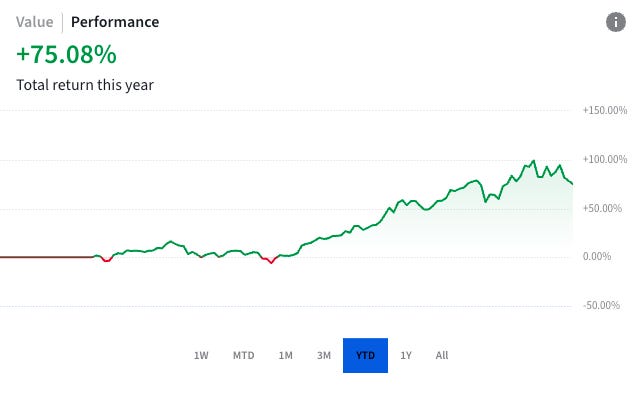

That brings us to the MS portfolio. We are more or less in line with where we were at the beginning of last month, with the MS portfolio up 75% YTD. Memory continues to be our strongest performer, with SK Hynix, Samsung, and Micron all performing exceptionally well.

MU -6.25%↓ trades around $1,050, roughly 8–9x forward earnings — versus Nvidia’s ~30x trailing multiple, for a company that’s just as levered to AI capex. The gap exists because investors still expect memory prices to crash as they did before.

The Strategic Capacity Agreements (SCAs) are Micron’s direct answer to that skepticism: floor pricing through 2030 for a significant share of its supply, signed by the same hyper-scalers and automakers. We believe the market is still not pricing this long-term structural shift in memory demand and profitability for the next 3-5 years.

As we highlighted last week, we will continue to hold these names and expect them to rise further as the market digests the impact of long-term contracts and becomes less concerned about the cyclicality of memory stocks.

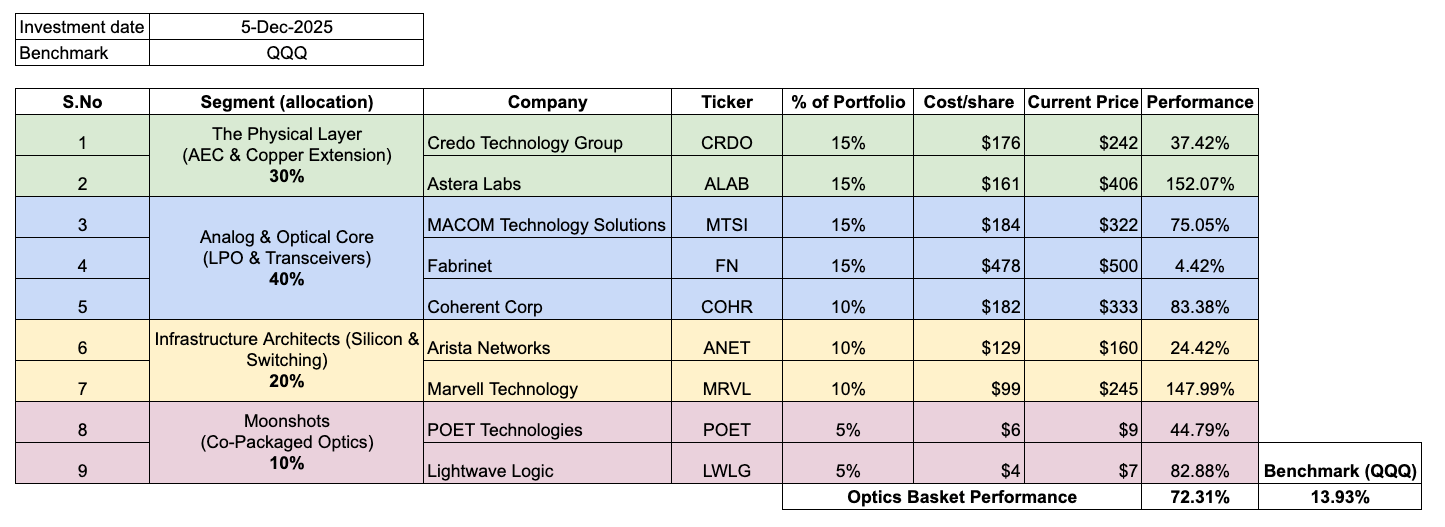

Update on Optics

Our Optics basket was a bet on AI data centers hitting the “Copper Wall”, a physical limit beyond which copper cables cannot transmit data fast enough over a given distance.

Existing high-speed copper cables can transmit data at 112 Gbps over a distance of 2 meters. The next generation of servers is projected to run at twice that speed, and at that point traditional passive copper will no longer reliably carry a signal across a server rack.

The basket was built intentionally to get exposure to both approaches being developed to overcome this problem:

Add signal boosters to existing copper data cables (Active Electrical Cables)

Convert the electrical signal into an optical signal, achieving near-perfect transition (Co-Packaged Optics – CPO)

Since its launch (Dec’25), our Optics basket is now up 72% vs 14% of QQQ. This outperformance was driven by AEC volumes scaling faster than planned: in the most recent quarter, Credo Technology Group reported ~150% YoY revenue growth and Astera Labs ~90%.

While AEC volume scaled, our optical bets also got several validating events:

Nvidia announced a multibillion‑dollar purchase commitment for Co-Packaged Optics along with a $2B investment in Coherent.

Arista Networks also launched XPO-MSA, a switch that uses removable optical connectors. It’s a stepping stone toward denser optical connections while the industry works toward fully integrated optics (CPO).

AEC companies benefit from mature products and are expected to grow by ~60%-80% through 2027, with a strong outlook through 2030. CPO companies are expected to grow ~30%-40% in 2027 as their initial product scales, with potential for better growth over the long run.

Post this strong rally, most portfolio companies in our basket are trading above 100 TTM P/E. Given this, we are updating the optics basket from Buy to Hold.